3D Semiconductor Packaging Market Report

Introduction:

The 3D semiconductor packaging market

has gained significant traction in recent years, driven by the demand for

high-performance, miniaturized, and energy-efficient electronic components.

Traditional 2D packaging methods are increasingly inadequate for meeting the

performance and space requirements of modern applications, leading to the rapid

adoption of 3D packaging technologies. These techniques allow multiple

integrated circuits (ICs) or dies to be stacked vertically, interconnected with

through-silicon vias (TSVs), micro bumps, or other advanced interconnects. The

result is enhanced functionality within a smaller footprint, reduced power

consumption, and improved overall performance.

3D semiconductor packaging is increasingly becoming essential in sectors such as consumer electronics, telecommunications, automotive, and data centers. With the proliferation of 5G, artificial intelligence (AI), and the Internet of Things (IoT), the demand for compact yet powerful semiconductor solutions is at an all-time high. Moreover, the surge in electric vehicles (EVs) and advanced driver-assistance systems (ADAS) has further fueled market growth.

The market is also seeing advancements in heterogeneous integration, where different types of chips such as logic, memory, and sensors are integrated into a single package, boosting system performance and enabling innovative applications. Research and development investments and government initiatives aimed at enhancing semiconductor manufacturing capabilities are acting as additional catalysts.

As we move toward more data-intensive applications and smarter devices, 3D semiconductor packaging offers a crucial pathway for innovation. The market outlook remains promising, with continued investment in research, technological improvements, and increasing collaboration across the supply chain. This report delves into the core aspects of the 3D semiconductor packaging market, including its definition, scope, segmentation, key drivers and trends, regional dynamics, and prominent players shaping its future.

Definition:

3D semiconductor packaging

refers to the method of stacking and interconnecting multiple integrated

circuit (IC) dies vertically within a single semiconductor package. Unlike

traditional 2D packaging where components are placed side-by-side on a

substrate, 3D packaging allows for greater functional density, enhanced

performance, and reduced power consumption. This architecture achieves vertical

integration using technologies such as through-silicon vias (TSVs),

micro-bumps, and interposers.

TSVs are vertical electrical connections that pass through silicon wafers or dies, facilitating communication between the stacked dies. Other methods such as wafer-level packaging (WLP), flip-chip technology, and hybrid bonding are also instrumental in enabling 3D packaging. These methods reduce interconnect length, minimize signal loss, and improve thermal management—making them suitable for high-speed and high-power applications.

3D semiconductor packaging can be classified into various types such as 3D system-in-package (3D SiP), 3D wafer-level chip-scale package (3D WLCSP), and 3D integrated circuits (3D ICs), each differing in design complexity and application. While 3D SiP focuses on integrating multiple functional chips into one package, 3D ICs involve stacking multiple active layers interconnected with TSVs.

The importance of 3D packaging lies in its ability to meet the demands of modern electronic devices, including smartphones, tablets, wearables, data centers, and autonomous vehicles. These devices require smaller form factors, faster processing capabilities, and efficient power usage—all of which are addressed by 3D packaging.

In essence, 3D semiconductor packaging represents a paradigm shift in the design and assembly of electronic systems. It is not merely an incremental improvement but a foundational technology that enables the next generation of high-performance, miniaturized electronic devices.

Scope & Overview:

The scope of the 3D semiconductor packaging market encompasses the full value

chain—from design and material development to fabrication, assembly, and final

application. It includes various packaging techniques, such as through-silicon

via (TSV) integration, 3D system-in-package (SiP), 3D wafer-level chip-scale

packaging (WLCSP), and 3D integrated circuits (ICs). These packaging forms

serve multiple sectors including consumer electronics, automotive,

telecommunications, healthcare, aerospace, and industrial automation.

The market is expanding due to rising demand for performance-intensive yet compact solutions in computing, communication, and automotive systems. As electronic devices evolve to support faster processing, greater storage, and improved functionality within smaller footprints, 3D semiconductor packaging becomes increasingly essential. It provides a scalable solution to overcome the limitations of Moore’s Law and meets the growing performance needs without significantly increasing chip area or power consumption.

Emerging technologies such as artificial intelligence (AI), machine learning, 5G networks, and edge computing are creating new opportunities for the adoption of 3D packaging solutions. The trend toward heterogeneous integration—combining logic, memory, and sensor functions into a single module—is accelerating adoption, especially for applications requiring high bandwidth and low latency.

The overview of the market also includes an analysis of supply chain components such as raw material suppliers, equipment manufacturers, OSAT (outsourced semiconductor assembly and test) providers, and end-user industries. A focus on sustainability and efficient heat dissipation has also led to innovation in packaging materials and thermal interface solutions.

In summary, the 3D semiconductor packaging market is poised for substantial growth driven by technological evolution and rising application demand across industries. The scope extends beyond mere packaging to serve as a critical enabler for next-generation electronics.

Size

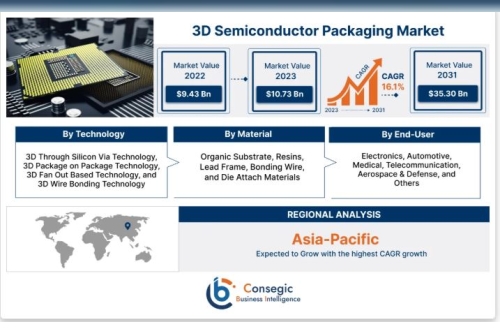

3D Semiconductor Packaging Market size is estimated to reach over USD 35.30 Billion by 2031 from a value of USD 9.43 Billion in 2022 and is projected to grow by USD 10.73 Billion in 2023, growing at a CAGR of 16.1% from 2023 to 2031.

Segmental Analysis:

By

Technology

3D Through Silicon Via Technology, 3D Package on Package Technology, 3D Fan Out Based Technology, and 3D Wire Bonding Technology

By Material

Organic Substrate, Resins, Lead Frame, Bonding Wire, and Die Attach Materials

By End-User

Electronics, Automotive, Medical, Telecommunication, Aerospace & Defense, and Others

Key Industry Drivers &

Trends:

The 3D semiconductor packaging market is being shaped by several compelling

drivers and emerging trends.

Key Drivers:

Miniaturization and Performance Needs: As devices become smaller and more powerful, there is an increased need for compact packaging solutions that offer higher performance and functionality within limited space. Demand for AI and 5G Applications: High-performance computing applications like AI and 5G require faster data transfer and lower latency, both of which are supported by 3D integration techniques. Electric and Autonomous Vehicles: The automotive industry's transition to electric and autonomous platforms demands robust and high-performance chips, thereby driving 3D packaging demand. Thermal Efficiency and Power Consumption: Improved heat dissipation and energy efficiency offered by 3D packaging technologies are vital for advanced electronics.Key Trends:

Heterogeneous Integration: Combining different types of chips (logic, memory, sensor) within one package is enabling more capable and efficient systems, especially in AI and mobile devices. Advanced Interconnect Technologies: The development of micro-bumps, hybrid bonding, and TSVs is pushing the limits of bandwidth and performance in semiconductor packaging. Growth of Foundry and OSAT Collaboration: Increasing collaborations across the supply chain are improving integration and reducing time-to-market. Sustainability and Reliability: There's a growing trend toward eco-friendly packaging materials and solutions that enhance reliability under varying operational conditions.Together, these drivers and trends are fostering rapid growth in the 3D semiconductor packaging market, setting the stage for continued innovation.

Regional Analysis:

The 3D semiconductor packaging market demonstrates diverse regional dynamics

shaped by manufacturing capabilities, technological innovation, and end-user

demand.

Asia-Pacific:

Asia-Pacific dominates the global market, led by countries like China, South

Korea, Taiwan, and Japan. The region’s stronghold in semiconductor fabrication

and electronic manufacturing, combined with significant R&D investment and

government support, fuels its leadership position. Consumer electronics and 5G

infrastructure deployment further amplify market demand.

North America:

North America is a major contributor, driven by its robust technological

ecosystem and demand for AI, IoT, and data center applications. The region

benefits from advanced R&D infrastructure and increasing investments in

chip design and fabrication. The automotive sector, especially with the push

toward electric vehicles, also supports market expansion.

Europe:

Europe’s market is growing steadily, supported by developments in automotive

electronics, industrial automation, and aerospace. Countries like Germany and

France are focusing on semiconductor innovation as part of their broader

digitalization and sustainability strategies.

Latin America and Middle

East & Africa:

These regions represent emerging markets with growing investments in smart

infrastructure, mobile connectivity, and automotive applications. Although

relatively smaller, the increasing adoption of high-performance electronics in

these areas provides potential for future growth.

Overall, regional growth patterns highlight the strategic importance of 3D semiconductor packaging in supporting national technological agendas and industrial competitiveness.

Key Players:

Amkor Technology, ASE Technology Holding Co. Ltd, Siliconware Precision

Industries Co. Ltd, JCET Group, Intel Corporation, Taiwan Semiconductor

Manufacturing Company Limited, Sony Corporation, Samsung, 3M, Advanced Micro

Devices Inc.

Contact Us:

Consegic Business intelligence

Email : [email protected]

Sales : [email protected]