Anti-seize Compounds Market Introduction

The global anti-seize compounds market has seen a steady rise in demand owing to the increasing need for effective lubrication and corrosion prevention in industrial applications. These compounds are essential for ensuring the longevity and performance of equipment exposed to high temperatures, corrosive environments, and mechanical wear. Industries such as automotive, marine, construction, aerospace, and manufacturing utilize anti-seize formulations to prevent the galling, seizing, and corrosion of metal components during assembly and operation. As industrial infrastructure grows worldwide, especially in emerging economies, the adoption of preventive maintenance materials like anti-seize compounds is becoming increasingly critical.

The market is being driven by factors such as growing industrialization, an increasing focus on preventive maintenance strategies, and rising awareness of equipment efficiency and operational safety. Moreover, the trend toward sustainability and environmentally friendly formulations is influencing product development, pushing manufacturers to innovate with non-metallic, biodegradable, and low-toxicity alternatives. Anti-seize compounds are now offered in various types such as copper-based, aluminum-based, nickel-based, and non-metallic versions to cater to specific operational needs across diverse environments.

Despite the favorable outlook, the market does face certain challenges. These include stringent environmental regulations regarding metal-based formulations and the potential for product misapplication, which can affect performance and safety. Nevertheless, ongoing research and development efforts aimed at improving compound efficiency, temperature resistance, and environmental compliance are expected to support continued growth. As industries increasingly seek robust solutions to minimize downtime and maximize asset durability, the anti-seize compounds market is likely to maintain a positive trajectory in the foreseeable future.

Anti-seize Compounds Market Definition

Anti-seize compounds are specialty lubricants designed to prevent the seizing, galling, and corrosion of metal components subjected to extreme conditions such as high temperatures, heavy loads, and corrosive environments. These compounds are typically applied to threaded connections, flanges, gaskets, and other metal-to-metal interfaces to facilitate easier disassembly, reduce wear, and ensure long-term equipment reliability.

The composition of anti-seize compounds usually includes a thickening agent or grease base combined with solid lubricants such as metallic powders (e.g., copper, aluminum, or nickel), graphite, or other synthetic materials. These materials create a protective layer between metal surfaces, reducing friction and preventing the formation of rust or oxidation. Some formulations are designed for general-purpose applications, while others are specifically tailored for extreme heat, pressure, or chemical exposure.

Anti-seize compounds are distinct from conventional lubricants in that they are formulated to remain stable and effective under conditions that would degrade or burn off standard greases or oils. For instance, high-temperature variants can function effectively at temperatures exceeding 1,200°C, making them suitable for applications in engines, turbines, and exhaust systems. Additionally, anti-seize compounds provide long-lasting protection against moisture and harsh environmental factors, making them vital in industries with outdoor or marine exposure.

While widely used in maintenance operations, these compounds also play an important role during the assembly phase of equipment manufacturing, ensuring that critical fasteners can be easily removed for inspection, repair, or replacement without damage. As the industrial landscape grows more complex and demanding, the functional importance of anti-seize compounds becomes increasingly evident. Their ability to reduce maintenance costs, enhance equipment life, and improve safety makes them an indispensable tool in both routine and high-performance industrial settings.

Anti-seize Compounds Market Scope & Overview

The anti-seize compounds market encompasses a broad range of products designed to protect metal surfaces from seizing, galling, rust, and corrosion under extreme operational conditions. These products are widely used across multiple sectors including automotive, aerospace, marine, construction, manufacturing, and power generation. The market caters to both OEM (original equipment manufacturer) and aftermarket applications, offering solutions that ensure mechanical reliability and operational efficiency.

The scope of the market covers different types of formulations, including metallic and non-metallic compounds, each serving specific temperature, pressure, and environmental conditions. Metallic-based compounds, such as those containing copper, aluminum, or nickel, are particularly valued for their high thermal conductivity and pressure resistance. Non-metallic or synthetic variants are gaining popularity due to their environmentally friendly attributes and non-reactive properties, which make them suitable for use on sensitive equipment or in food-grade environments.

The market is influenced by growing industrial automation and the expanding footprint of manufacturing and infrastructure development in emerging economies. Increased awareness of asset lifecycle management and the benefits of preventive maintenance are further driving the demand for anti-seize solutions. Furthermore, the shift towards electric vehicles and clean energy has introduced new use cases for anti-seize materials in battery assemblies, electrical fittings, and renewable energy equipment.

From a technological standpoint, advancements in compound formulations are leading to better performance characteristics, such as higher temperature thresholds, broader compatibility with dissimilar metals, and resistance to aggressive chemicals. Digitalization and smart maintenance practices are also contributing to the adoption of high-performance anti-seize products in predictive maintenance programs.

In essence, the anti-seize compounds market is a critical segment of the broader industrial lubrication and maintenance industry. Its evolving applications and technological advancements are positioning it for consistent growth and innovation.

Anti-seize Compounds Market Size

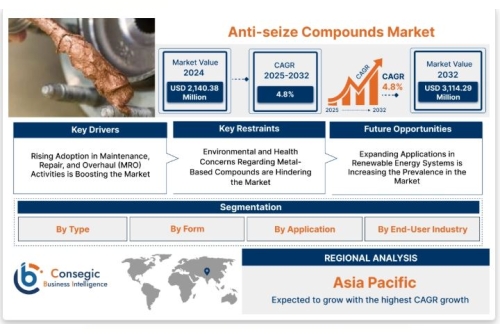

Anti-seize Compounds Market size is estimated to reach over USD 3,114.29 Million by 2032 from a value of USD 2,140.38 Million in 2024 and is projected to grow by USD 2,204.98 Million in 2025, growing at a CAGR of 4.8% from 2025 to 2032.

Anti-seize Compounds Market Segmental Analysis

By Type

Copper-Based Anti-Seize Compounds Nickel-Based Anti-Seize Compounds Aluminum-Based Anti-Seize Compounds Zinc-Based Anti-Seize Compounds Non-Metallic Anti-Seize Compounds OthersBy Form

Paste Liquid AerosolBy Application

Threaded Connections Gaskets Bearings Valves OthersBy End-Use Industry

Automotive Aerospace Marine Industrial Equipment Construction Oil & Gas OthersAnti-seize Compounds Market Key Industry Drivers & Trends

The anti-seize compounds market is influenced by a combination of industrial, environmental, and technological factors that are driving growth and innovation. One of the primary drivers is the increasing emphasis on preventive maintenance across industries. As downtime and equipment failure become costlier, companies are investing in reliable maintenance products, with anti-seize compounds playing a key role in extending component life and simplifying disassembly.

The continued growth of key end-use sectors such as automotive, aerospace, and manufacturing is also contributing significantly to market demand. As these industries expand globally, the requirement for high-performance lubricants that can withstand heat, pressure, and corrosion becomes more critical. Additionally, the rise in infrastructure projects, particularly in emerging economies, is fueling the need for dependable anti-seize products in construction and heavy machinery applications.

Environmental regulations are shaping the market by encouraging the development of eco-friendly and non-metallic anti-seize formulations. This shift aligns with broader sustainability goals and the global push for reducing heavy metal content in industrial products. Non-metallic compounds, which are often free from lead, copper, or other harmful materials, are gaining traction for their safety and compliance benefits.

Another emerging trend is the integration of anti-seize compounds into predictive maintenance programs. With the rise of Industry 4.0 and smart manufacturing, data-driven maintenance practices are becoming the norm, and anti-seize materials are being chosen not just for their chemical properties but for their role in reducing repair times and extending maintenance intervals.

Overall, the market is experiencing a transition toward high-performance, environmentally responsible products, while maintaining its core function—enhancing reliability and reducing maintenance costs. These evolving trends are positioning anti-seize compounds as a vital component in modern industrial practices.

Anti-seize Compounds Market Regional Analysis

The global anti-seize compounds market exhibits regional diversity in terms of demand, application areas, and regulatory influence. Industrial development, manufacturing intensity, and environmental regulations are key factors shaping regional dynamics.

North America holds a significant share of the market, driven by well-established automotive, aerospace, and heavy machinery industries. High standards for maintenance and safety, coupled with strict environmental regulations, have led to a strong preference for high-performance and eco-friendly formulations. The presence of a mature aftermarket service network further contributes to steady product demand.

Europe is another prominent region, with growth supported by strong industrial activity, particularly in Germany, France, and the UK. The region’s emphasis on sustainability and compliance with REACH (Registration, Evaluation, Authorisation and Restriction of Chemicals) regulations is fostering demand for non-metallic and biodegradable compounds. Europe's renewable energy expansion also contributes to new applications for anti-seize products.

Asia Pacific is the fastest-growing region, propelled by rapid industrialization, expanding automotive production, and rising infrastructure investment in countries like China, India, and Southeast Asia. As these economies mature, there is a growing emphasis on adopting preventive maintenance practices, increasing the adoption of anti-seize compounds in both OEM and aftermarket segments.

Latin America and the Middle East & Africa are emerging markets with considerable potential. Growth in construction, mining, and energy sectors is driving demand, though the adoption rate may be affected by lower awareness and cost sensitivity. However, as industrial activity picks up and regulatory frameworks become more structured, these regions are likely to contribute increasingly to the global market.

Overall, while developed regions continue to demand high-specification, compliant products, emerging markets offer opportunities for expansion through infrastructure development and industrial growth.

Anti-seize Compounds Market Key Players

Henkel AG & Co. KGaA (Germany)

The Dow Chemical Company (USA)

3M Company (USA)

SKF Group (Sweden)

Rocol (UK)

FUCHS (Germany)

DuPont (USA)

Bostik (France)

CSW Industrials, Inc. (USA)

CRC Industries (USA)

Contact Us:

Consegic Business intelligence

Email : [email protected]

Sales : [email protected]