Automotive Engine Valve Market Report

Introduction

The automotive engine valve market

is a critical segment of the global automotive component industry, driven by

the growing demand for fuel-efficient, high-performance, and environmentally

friendly vehicles. Engine valves are essential mechanical components that

control the intake of air and fuel as well as the expulsion of exhaust gases in

internal combustion engines. As automotive manufacturers innovate with more

complex engine designs, including variable valve timing and turbocharging, the

need for advanced valve technologies is rising. This trend is especially

prevalent in light of increasingly stringent emissions and fuel economy

regulations worldwide.

The global rise in vehicle production, particularly in emerging economies, is significantly contributing to market expansion. Additionally, the automotive industry's ongoing transition toward hybrid and electric vehicles is influencing innovations in valve materials and design, even as it gradually shifts the demand landscape. While electric vehicles may eventually reduce the need for traditional engine valves, hybrid vehicles still rely on combustion engines, sustaining demand in the interim.

Further, the aftermarket segment plays a pivotal role in the market dynamics, with vehicle maintenance and repair driving consistent demand for engine valve replacements. Advancements in materials, such as titanium and sodium-filled valves, are enhancing performance, thermal resistance, and durability, helping OEMs meet performance expectations under stringent environmental constraints.

Overall, the automotive engine valve market remains a dynamic space shaped by regulatory pressures, technological advancements, and evolving vehicle platforms. While long-term electrification trends may pose challenges, the near-to-mid-term prospects remain strong due to global automotive output and innovation in combustion engine technology. Investments in research and development, along with strategic supply chain optimizations, are expected to characterize market strategies moving forward.

Definition

An automotive engine valve

is a mechanical component integrated into an internal combustion engine to

regulate the flow of gases into and out of the engine’s combustion chambers or

cylinders. There are primarily two types of valves in such engines: intake

valves and exhaust valves. The intake valve opens to allow the air-fuel mixture

to enter the combustion chamber, while the exhaust valve opens to expel

combustion gases after the power stroke.

Engine valves operate in a precise sequence, synchronized with the engine’s camshaft and crankshaft, ensuring optimal engine performance and efficiency. Their ability to withstand high pressure, temperature, and friction is critical to an engine’s overall functionality and longevity. Typically manufactured using materials like steel alloys, stainless steel, or titanium, engine valves are engineered to endure harsh conditions while delivering smooth engine operation.

Valves may vary in design, such as poppet valves, sleeve valves, and rotary valves, although poppet valves are the most commonly used in modern vehicles. These valves have a mushroom-shaped head and move up and down in a reciprocating motion to open or close the passageways in the cylinder head.

Advanced automotive engines may incorporate variable valve timing (VVT) technologies, which allow for optimized valve opening and closing based on engine load and speed. This enhances performance, improves fuel efficiency, and reduces emissions. Sodium-filled valves, often used in performance or heavy-duty engines, enhance heat dissipation and valve longevity.

In essence, the automotive engine valve is a core component that plays a vital role in controlling engine breathing, combustion efficiency, and emission control. As engine designs evolve to meet new regulatory and performance requirements, the demand for reliable, durable, and technologically advanced engine valves continues to grow across the automotive industry.

Scope & Overview

The automotive engine valve market encompasses the development, manufacturing,

and supply of intake and exhaust valves for use in internal combustion engines

across a range of vehicle types, including passenger cars, commercial vehicles,

and two-wheelers. The scope of the market includes both original equipment

manufacturer (OEM) demand as well as the aftermarket for valve replacements and

upgrades.

Technological advancements, evolving emission norms, and the global push toward fuel-efficient vehicles are shaping the market's future. With modern internal combustion engines becoming increasingly complex, demand for valves that offer high precision, lightweight characteristics, and thermal resistance is rising. The market also includes components like valve guides, valve seats, and associated actuation systems, which work together to ensure valve reliability and performance.

Innovation is driving expansion into new material compositions such as titanium alloys, nickel-based superalloys, and sodium-filled valves to meet high-performance engine requirements. Further, integration with advanced engine technologies, including turbocharging and VVT systems, has broadened the scope of valve design and manufacturing.

From an application standpoint, the market extends across gasoline and diesel engine platforms. However, with growing popularity of hybrid vehicles, the relevance of engine valves remains intact even as full electrification looms. The market also reflects a growing shift in consumer preference toward smaller displacement engines, which typically demand more efficient and durable valve systems.

Geographically, the market spans North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa, with Asia Pacific dominating due to high vehicle production rates. The automotive engine valve market, therefore, represents a mature yet innovative segment of the broader automotive parts industry, continually adapting to technological progress and regulatory mandates.

As the automotive landscape evolves, the engine valve market must align with trends in electrification, lightweighting, and emission control, ensuring its continued relevance and growth over the forecast period.

Size

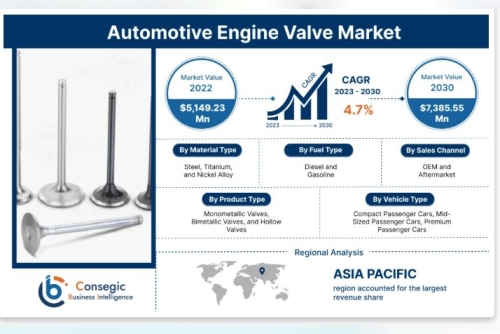

Global Automotive Engine Valve Market size is estimated to reach over USD 7,385.55 Million by 2030 from a value of USD 5,149.23 Million in 2022, growing at a CAGR of 4.7% from 2023 to 2030.

Segmental Analysis

By Product Type

Monometallic Valves, Bimetallic Valves, and Hollow Valves

By Vehicle Type

Compact Passenger Cars, Mid-Sized Passenger Cars, Premium Passenger Cars

By Material Type

Steel, Titanium, and Nickel Alloy

By Fuel Type

Diesel and Gasoline

By Sales Channel

OEM and Aftermarket

Key Industry Drivers &

Trends

The automotive engine valve market is shaped by a combination of technological

evolution, regulatory mandates, and shifting consumer preferences. One of the

primary market drivers is the continued global demand for fuel-efficient and

high-performance vehicles. As governments impose stringent emissions

regulations, automotive manufacturers are compelled to enhance engine

performance and combustion efficiency, directly influencing engine valve design

and demand.

Another key driver is the proliferation of variable valve timing (VVT) and turbocharged engines. These technologies require more sophisticated and durable valves that can perform reliably under varying loads and higher temperatures. As a result, the market is witnessing growing interest in materials such as titanium and sodium-filled valves for their heat-resistance and lightweight properties.

The surge in passenger car production, particularly in emerging markets, significantly boosts engine valve consumption. Additionally, the longevity of vehicle ownership in various countries is sustaining demand in the aftermarket segment, as aging engines require valve replacements and refurbishments.

A notable trend is the increasing focus on lightweight materials and manufacturing innovations to reduce engine weight and improve fuel economy. This aligns with the broader industry trend toward vehicle electrification and sustainability. While electric vehicles (EVs) do not use engine valves, the transition is gradual, and hybrid vehicles continue to rely on internal combustion engine components.

Digital integration and precision manufacturing technologies, including CNC machining and 3D printing, are also contributing to enhanced valve production capabilities, ensuring consistency, performance, and customization.

Moreover, the push toward downsized engines with higher efficiency levels is creating demand for valves capable of handling greater pressures and thermal stress. These trends underscore a market in transition—innovating within traditional boundaries while preparing for future shifts driven by electrification and changing mobility patterns.

Overall, the market remains resilient due to its foundational role in engine mechanics and the ongoing evolution of combustion engine technologies.

Regional Analysis

The automotive engine valve market exhibits varied growth dynamics across

global regions, shaped by differences in automotive production volumes,

regulatory environments, and technological adoption.

Asia Pacific dominates the global market, driven by high vehicle production rates in countries such as China, India, Japan, and South Korea. This region benefits from robust OEM presence, increasing domestic automotive demand, and favorable government policies supporting manufacturing. The rising disposable incomes and expanding middle class further bolster the passenger car market, thereby fueling engine valve consumption.

North America holds a significant market share, supported by a strong automotive manufacturing base and a well-established aftermarket ecosystem. Technological innovation and the demand for high-performance and fuel-efficient engines sustain growth in the region. Stricter emission norms from environmental agencies also compel OEMs to upgrade engine valve systems.

Europe remains a vital region due to its advanced automotive industry and aggressive environmental regulations. The market here is driven by the push toward downsized engines and hybrid powertrains. European automakers are at the forefront of innovation, particularly in valve materials and advanced actuation systems. However, the region's gradual shift toward electrification could temper future growth in traditional engine valve segments.

Latin America and the Middle East & Africa represent emerging markets, offering moderate growth opportunities. In Latin America, Brazil and Mexico are notable contributors due to localized vehicle production and a growing demand for replacement parts. In the Middle East & Africa, economic diversification, increasing vehicle imports, and infrastructural development are supporting automotive component demand.

Overall, regional growth is contingent on factors such as production trends, regulatory pressures, economic development, and the pace of electrification. While mature markets are gradually shifting toward hybrid and electric mobility, emerging economies continue to sustain demand for conventional engine technologies, ensuring balanced growth in the automotive engine valve market globally.

Key Players

Continental AG, Cummins, BorgWarner, Denso Corporation, Eaton Corporation PLC,

Federal-Mogul Holdings Corp, FTE Automotive GmBH, Hitachi Ltd., Johnson

Electric Group, Knorr-Bremse AG, Robert Bosch GmbH, Schaeffler AG

Contact Us:

Consegic Business intelligence

Email : [email protected]

Sales : [email protected]

Furnished 1-Bhk Apt Rent in Bashundhara R/A,Dhaka

Furnished 1-Bhk Apt Rent in Bashundhara R/A,Dhaka