Data Center Structured Cabling Market Report

Introduction:

The Data Center Structured Cabling

Market is witnessing robust growth driven by the

rising demand for high-speed connectivity, increased data traffic, and

expansion of cloud-based services. Structured cabling forms the critical

backbone of modern data centers, enabling efficient data flow, scalability, and

simplified network management. As digital transformation accelerates across

industries, organizations are investing heavily in data centers to manage and

store massive volumes of data, thereby creating significant opportunities for

structured cabling solutions. This market benefits from the ongoing

proliferation of technologies such as 5G, IoT, AI, and big data analytics,

which require high-bandwidth and low-latency infrastructure.

The demand for scalable and high-performance cabling systems has increased due to the shift towards hyper-scale and edge data centers. Enterprises prioritize solutions that offer minimal downtime, operational efficiency, and adaptability to future upgrades. Structured cabling, with its standardized approach, supports these requirements by reducing complexity and ensuring seamless integration of network components. Moreover, rising concerns about data security, regulatory compliance, and uptime reliability further emphasize the importance of robust cabling infrastructure.

Technological advancements, including the adoption of Category 6A and fiber optic cabling, have enhanced transmission speeds and reliability, further strengthening the market outlook. Governments and private enterprises alike are investing in digital infrastructure, particularly in emerging economies, which is projected to significantly boost market expansion. Overall, the Data Center Structured Cabling Market is poised for substantial growth, shaped by dynamic industry demands and technological progress.

Definition:

Data center structured cabling

refers to the standardized system of cabling and associated hardware used to

provide comprehensive telecommunications infrastructure in data centers. This

infrastructure supports a wide array of applications including voice, data,

video, and various management systems. The structured approach involves a

hierarchical design, with components such as entrance facilities, main

distribution areas (MDA), horizontal distribution areas (HDA), and equipment

distribution areas (EDA), all organized to support a modular and scalable

architecture.

Structured cabling in data centers is engineered for reliability, manageability, and efficiency. Unlike traditional point-to-point cabling, structured systems offer centralized management and a high degree of flexibility, which allows for quick reconfigurations and future scalability without major overhauls. The use of industry-recognized standards, such as those established by TIA/EIA and ISO/IEC, ensures uniformity and interoperability across components and vendors.

This system typically incorporates copper cables (like Category 5e, 6, 6A) and fiber optic cables (single-mode and multi-mode), chosen based on data speed requirements, distance, and environmental conditions. The adoption of high-density fiber connectivity is increasingly prevalent due to its capacity to handle large data volumes in a compact footprint. As data centers continue evolving toward higher speeds and greater virtualization, structured cabling plays a crucial role in ensuring performance, reducing latency, and simplifying maintenance.

In essence, data center structured cabling is not merely about wiring, but a foundational technology that underpins reliable, scalable, and efficient data center operations. It ensures seamless communication between servers, storage devices, switches, and other network equipment, making it indispensable for today’s digital infrastructure.

Scope & Overview:

The scope of the Data Center Structured Cabling Market encompasses a wide range

of products, services, and solutions tailored for efficient and future-ready

data center infrastructure. This market includes cabling types such as copper

and fiber optics, supporting accessories, design and installation services, and

ongoing maintenance. Structured cabling is used across various data center

environments including enterprise, colocation, and hyperscale facilities, each

with distinct infrastructure needs and scalability demands.

The market is influenced by a shift toward high-speed transmission networks to support the exponential growth in data generation and cloud services. As organizations increasingly migrate workloads to the cloud, data centers require structured cabling systems that can manage increased traffic with reliability and minimal latency. Consequently, there is a strong focus on upgrading legacy cabling systems with high-performance solutions that support 10G, 40G, 100G, and beyond.

The market also extends to verticals such as IT & telecom, BFSI, healthcare, government, and energy, all of which are experiencing increased digitization. Structured cabling solutions are designed to offer high availability and redundancy, supporting mission-critical operations in these sectors. Additionally, the adoption of green data center concepts and energy-efficient solutions has led to innovations in cabling materials and designs that minimize power loss and heat generation.

Overall, the Data Center Structured Cabling Market offers comprehensive infrastructure solutions designed to enhance network performance, scalability, and manageability. With growing investments in data center expansion and modernization, the market is expected to register consistent growth and evolution over the coming years.

Size

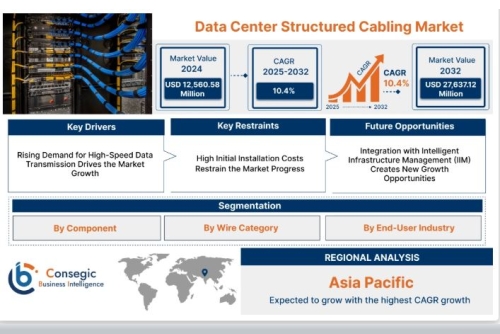

Data Center Structured Cabling Market size is estimated to reach over USD 27,637.12 Million by 2032 from a value of USD 12,560.58 Million in 2024 and is projected to grow by USD 13,638.05 Million in 2025, growing at a CAGR of 10.4% from 2025 to 2032.

Segmental Analysis:

By Component

By Wire Category

Category 5E Category 6 Category 6A Category 7 OthersBy End-User Industry

IT & Telecom BFSI Healthcare Retail & E-Commerce Manufacturing Government Others

Key Industry Drivers &

Trends:

Several key drivers and trends are propelling the growth of the Data Center

Structured Cabling Market. One of the primary drivers is the increasing demand

for high-speed and low-latency data transmission to support cloud computing,

big data analytics, and real-time applications. Organizations require efficient

and scalable network infrastructure, which structured cabling readily provides.

The expansion of hyperscale and edge data centers is another critical growth factor. Hyperscale facilities need dense and robust cabling infrastructure to support massive volumes of data and multiple connections. Meanwhile, edge data centers, which aim to reduce latency by bringing computation closer to end-users, are also investing in flexible structured cabling systems for rapid deployment and operational efficiency.

A significant trend is the growing adoption of fiber optic cabling over traditional copper cabling due to its superior performance and energy efficiency. Fiber optics can support higher data rates over longer distances, making them ideal for modern data center architectures. Additionally, modular and high-density cabling systems are being embraced to maximize space utilization and simplify future upgrades.

Sustainability and energy efficiency have emerged as central themes, with organizations opting for eco-friendly cabling materials and designs that contribute to green data center initiatives. Moreover, increasing awareness around network reliability, disaster recovery, and uptime assurance has emphasized the need for organized and standards-compliant cabling solutions.

Another emerging trend is the integration of intelligent cabling systems that incorporate sensors and automation for real-time monitoring, fault detection, and performance optimization. These smart systems enhance operational visibility and help in proactive maintenance, reducing downtime and boosting efficiency.

Regional Analysis:

The Data Center Structured Cabling Market shows a varied regional outlook, with

distinct growth patterns across North America, Europe, Asia Pacific, Latin

America, and the Middle East & Africa.

North America leads the market due to the widespread adoption of digital technologies, established data center infrastructure, and continuous investments in hyperscale data centers. The region's emphasis on 5G, AI, and IoT applications has accelerated the need for advanced cabling systems that ensure high-speed and reliable connectivity.

Europe follows closely, driven by stringent data privacy regulations, increased cloud adoption, and smart city initiatives. Countries like Germany, the UK, and the Netherlands are witnessing a surge in data center construction, propelling demand for structured cabling solutions that align with energy efficiency goals and regulatory standards.

The Asia Pacific region is expected to exhibit the fastest growth, fueled by rapid urbanization, digital transformation, and government initiatives to boost IT infrastructure. Major economies such as China, India, and Japan are experiencing increased demand for cloud services, e-commerce, and video streaming, requiring robust data center infrastructure supported by structured cabling.

Latin America is gradually developing its digital infrastructure, with Brazil and Mexico leading in data center investment. Growth in this region is supported by increasing internet penetration and enterprise digitization.

The Middle East & Africa are also witnessing growing interest in data center projects, particularly in the Gulf Cooperation Council (GCC) countries. Government-led diversification programs and smart city projects are encouraging investment in ICT infrastructure, thereby driving structured cabling adoption.

Key Players:

CommScope (USA)

Panduit (USA)

Corning Inc. (USA)

Legrand (France)

Nexans (France)

Schneider Electric (France)

Belden Inc. (USA)

Furukawa Electric Co., Ltd. (Japan)

R&M (Reichle & De-Massari AG) (Switzerland)

Siemon (USA)

Contact Us:

Consegic Business intelligence

Email : [email protected]

Sales : [email protected]

Fortinet NSE 4 – FortiOS 7.6 Administrator NSE4_FGT_AD-7.6 Dumps

Fortinet NSE 4 – FortiOS 7.6 Administrator NSE4_FGT_AD-7.6 Dumps