Interactive Video Wall Market Report

Introduction:

The Interactive Video Wall market has emerged as a transformative force in modern visual communication, bridging the gap between dynamic content presentation and real-time user interaction. Originally developed for high-end corporate and entertainment purposes, interactive video walls are now gaining prominence across various industries including education, retail, transportation, hospitality, and government. These systems integrate multiple display panels to form a single large-scale, seamless visual interface that supports touch, gesture, or sensor-based inputs, offering an immersive and engaging user experience. The increasing need for enhanced brand engagement, customer interaction, and digital transformation initiatives is fueling demand for these advanced display systems. Technological innovations in display resolution, touch sensitivity, and integration with AI and IoT platforms are accelerating market growth. Additionally, the shift toward remote collaboration and digital signage in the post-pandemic world is reinforcing the relevance of interactive video walls. As organizations aim to create impactful communication strategies and environments that captivate audiences, the market is poised for sustained expansion. Market players are also investing in software development, energy-efficient displays, and modular hardware designs to meet the evolving demands of diverse end-users. With growing applications in smart cities and command centers, the interactive video wall market is set to witness substantial opportunities in the coming years.

Definition:

An interactive video wall refers to a large visual display system composed of multiple screens or panels seamlessly tiled together to form a single expansive display surface that is capable of recognizing and responding to user inputs. Unlike traditional video walls that primarily serve as passive content display units, interactive video walls are embedded with technologies that facilitate user engagement through touch screens, gesture controls, or sensor-based input systems. These video walls can vary in size, configuration, and resolution, depending on the application and environment in which they are deployed. Typically powered by advanced display technologies such as LED, LCD, and OLED, these systems can deliver high-definition or ultra-high-definition visuals with superior brightness and clarity. The interactivity is enabled by software and hardware components such as multi-touch overlays, interactive controllers, and input management systems. These walls are often integrated with analytics platforms, content management systems, and collaboration tools to maximize their functionality in sectors like retail, education, healthcare, and public administration. They are used for interactive advertising, digital signage, data visualization, and real-time collaboration, providing users with engaging and intuitive experiences. As organizations increasingly seek tools that merge digital content with interactive experiences, interactive video walls are becoming a vital component of modern digital infrastructure.

Scope & Overview:

The scope of the interactive video wall market encompasses the development, integration, and deployment of high-definition modular display systems that facilitate user interaction through various input modalities. This market includes hardware such as display panels, interactive touch overlays, media controllers, and software for content management and interaction. It serves multiple industries including education, retail, corporate communication, healthcare, transportation, and public services. The global surge in demand for digital signage and smart display technologies is pushing the market toward rapid growth. Urbanization, the need for real-time data visualization, and enhanced public engagement are driving investments in interactive installations, particularly in smart city and command center projects. The market is also evolving with advancements in display resolutions (4K, 8K), touch technology (capacitive, infrared, optical), and integration with emerging technologies like AI, AR/VR, and IoT. From interactive museum exhibits to control rooms and smart classrooms, the breadth of application is expanding. Cloud-based content platforms, scalability, and improved durability of hardware are further enhancing market viability. Despite challenges like high initial costs and maintenance requirements, growing ROI awareness and technological maturity are mitigating these barriers. Overall, the interactive video wall market presents a robust opportunity for innovation and expansion in both public and private sectors.

Size

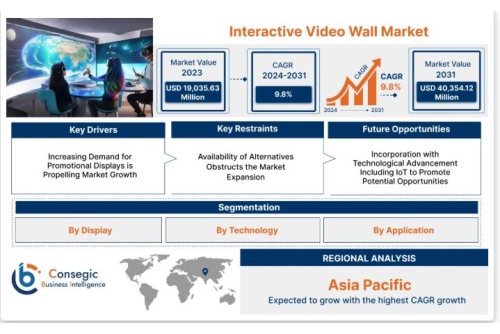

Interactive Video Wall Market size is estimated to reach over USD 40,354.12 Million by 2031 from a value of USD 19,035.63 Million in 2023 and is projected to grow by USD 20,571.04 Million in 2024, growing at a CAGR of 9.8% from 2024 to 2031.

Segmental Analysis:

By Display

LCD LED OLED OthersBy Technology

Touch-based Gesture-based Non-touch OthersBy Installation

BFSI Retail Transportation Commercial Government Entertainment Education Healthcare Others

Key Industry Drivers & Trends:

Several critical factors are driving the growth of the interactive video wall market. The rising demand for immersive and engaging user experiences is a major growth catalyst, particularly in sectors such as retail, education, and corporate communication. Organizations are increasingly leveraging video walls to captivate audiences, improve customer engagement, and enhance brand visibility. The proliferation of smart cities and digital infrastructure projects is accelerating the installation of interactive video walls in public spaces, transportation hubs, and control rooms. Technological advancements in display resolution, touch interfaces, and energy efficiency are improving the overall value proposition of interactive video walls. Integration with artificial intelligence, machine learning, and real-time analytics is also becoming a defining trend, enabling intelligent content adaptation based on user behavior. The rise of hybrid work environments and digital collaboration platforms is further encouraging businesses to invest in interactive visual communication tools. Cloud-based content management systems are streamlining deployment and scalability. In parallel, environmental concerns are pushing manufacturers toward sustainable and energy-efficient solutions. Another trend is the modular design of video walls that allow easy customization and maintenance. These industry dynamics collectively shape a market that is not only growing but evolving rapidly to meet the sophisticated demands of a digitally connected world.

Regional Analysis:

The interactive video wall market demonstrates distinct regional trends, shaped by technological maturity, infrastructure investment, and digital adoption rates. North America holds a significant share of the market, driven by widespread use in corporate environments, retail spaces, and public information systems. High technology adoption rates, coupled with robust IT infrastructure, support market expansion in this region. Europe follows closely, with a strong emphasis on interactive digital signage in education, transportation, and smart city projects. Countries like Germany, the UK, and France are notable contributors due to proactive government initiatives and private sector digitization. The Asia-Pacific region, however, is expected to witness the fastest growth, fueled by rapid urbanization, increasing smart city developments, and expanding digital ecosystems in countries such as China, India, South Korea, and Japan. These countries are increasingly adopting interactive technologies in both public and private sectors to enhance communication and engagement. The Middle East and Africa are gradually embracing video wall systems, particularly in high-profile commercial spaces, airports, and public installations. Latin America, although still developing in terms of adoption, is showing signs of potential growth with investments in retail and entertainment sectors. Overall, regional dynamics reflect a global shift toward more interactive and immersive digital experiences.

Key Players:

LG Electronics(Japan)

Samsung Electronics (South Korea)

NEC Corporation (Japan)

Delta Electronics, Inc (Taiwan)

Barco (Belgium)

Sony Corporation (Japan)

Philips N.V (Netherlands)

Planar (US)

Panasonic (Japan)

Christie Digital Systems (US)

Mitsubishi Corporation (Japan)

Formetco (US)

Contact Us:

Consegic Business intelligence

Email : [email protected]

Sales : [email protected]