Network Security Appliance Market Report

Introduction

The Network Security Appliance market

is emerging as a cornerstone in the modern digital infrastructure landscape. As

cyber threats grow in volume and sophistication, enterprises and institutions

are rapidly adopting hardware-based security solutions to protect critical data

and network resources. Network security appliances—encompassing firewalls,

intrusion prevention systems (IPS), unified threat management (UTM) devices,

and VPN concentrators—form an essential layer of defense in corporate IT

environments. The rising number of remote users, expansion of cloud services,

and rapid digitization across sectors have pushed organizations to seek

reliable and robust security infrastructure, thereby fueling the demand for

such appliances.

Amid growing concerns around data privacy regulations and compliance mandates globally, enterprises are increasingly deploying network security appliances not just at the core but also at the edge of their networks. Governments and regulatory bodies are mandating more rigorous cybersecurity frameworks, contributing further to market expansion. Additionally, the proliferation of Internet of Things (IoT) devices and the evolution of 5G technology are widening the attack surface for cybercriminals, thereby making traditional security approaches inadequate.

In this context, the global Network Security Appliance market is poised for significant growth, driven by the convergence of emerging technologies, security needs, and increased awareness. The industry is witnessing a shift towards integrated, automated, and AI-driven security appliances that can adapt to evolving threat landscapes. As digital transformation accelerates, particularly in SMEs and developing economies, the demand for cost-effective and scalable network security solutions is likely to experience robust growth. The market is characterized by innovation, with vendors continually enhancing performance, real-time threat intelligence, and policy enforcement capabilities. This report offers a comprehensive analysis of the Network Security Appliance market by exploring its definition, scope, segmentation, drivers, trends, regional landscape, and key players shaping the future of this vital domain.

Definition

Network Security Appliances

refer to dedicated hardware devices designed to protect computer networks from

unauthorized access, cyberattacks, and other security threats. These appliances

act as the first line of defense between an organization’s internal IT

infrastructure and external networks, such as the internet. Their primary role

is to monitor, detect, block, and respond to malicious traffic or unauthorized

data flows, ensuring the confidentiality, integrity, and availability of

digital assets.

Typically deployed at network gateways, these appliances perform a variety of functions including firewall filtering, intrusion detection and prevention (IDS/IPS), deep packet inspection, antivirus scanning, virtual private network (VPN) facilitation, and content filtering. Network security appliances can be standalone devices or part of integrated systems offering multiple layers of security functionality—commonly referred to as Unified Threat Management (UTM). These appliances are critical for enforcing security policies, monitoring network traffic, preventing data breaches, and complying with regulatory requirements such as GDPR, HIPAA, and PCI-DSS.

Modern network security appliances are equipped with advanced capabilities such as artificial intelligence, machine learning, cloud integration, and zero-trust network access (ZTNA). This evolution helps organizations address sophisticated threats like ransomware, advanced persistent threats (APTs), and phishing attacks more effectively. These appliances also offer centralized visibility and control over network security, enabling IT teams to swiftly respond to security incidents and maintain operational continuity.

Network Security Appliances are applicable across various sectors including finance, healthcare, government, education, and industrial settings. They are essential for both large enterprises and small to medium-sized businesses (SMBs), especially in the wake of rising remote work trends and expanding attack vectors. As such, these devices have become an indispensable part of the modern cybersecurity ecosystem.

Scope & Overview

The scope of the Network Security Appliance market encompasses a wide array of

hardware solutions engineered to safeguard digital infrastructure from external

and internal threats. These appliances provide foundational security functions

and are integral to maintaining a secure and resilient IT environment across

different scales of operations—from small offices to large-scale enterprise

networks. This market includes traditional and next-generation firewalls, UTM

devices, network intrusion prevention systems (IPS), and secure web gateways,

among others.

As enterprises become more reliant on digital tools and internet-based services, the importance of network security appliances has grown. The market serves diverse verticals such as financial services, healthcare, retail, manufacturing, telecommunications, government, and education. Key areas of focus within the market include on-premise deployment, hybrid cloud integration, and edge computing support, with appliances tailored to meet various throughput requirements and compliance standards.

The Network Security Appliance market operates within a dynamic cybersecurity landscape characterized by evolving threats, stringent regulatory requirements, and rapid technological advancement. The proliferation of remote work, bring-your-own-device (BYOD) policies, and increased adoption of cloud services have all contributed to heightened security vulnerabilities, thereby expanding the addressable market for these appliances. Simultaneously, technological advancements such as AI-driven threat detection, real-time analytics, and automated response mechanisms are transforming the functionality and efficiency of modern appliances.

This report provides a comprehensive overview of the market by examining key trends, regional developments, competitive dynamics, and segmentation based on product types, end-users, and deployment modes. With digital transformation accelerating globally, the demand for flexible, scalable, and intelligent network security appliances is expected to rise, positioning the market for sustained long-term growth and innovation.

Size

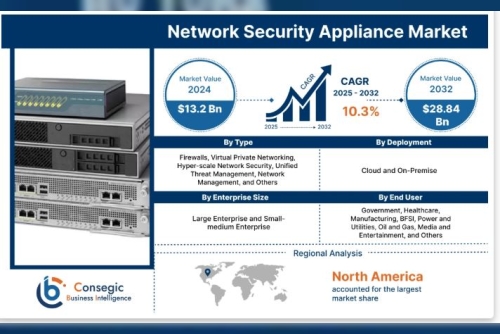

Network Security Appliance Market Size is estimated to reach over USD 28.84 Billion by 2032 from a value of USD 13.2 Billion in 2024, growing at a CAGR of 10.3% from 2025 to 2032.

Segmental Analysis

By Type

Firewalls, Virtual Private Networking, Hyper-scale Network Security, Unified Threat Management, Network Management, and Others

By Deployment

Cloud and On-Premise

By Enterprise Size

Large Enterprise and Small-medium Enterprise

By End-User

Government, Healthcare, Manufacturing, BFSI, Power and Utilities, Oil and Gas, Media and Entertainment, and Others

Key Industry Drivers &

Trends

The growth of the Network Security Appliance market is underpinned by several

key drivers and trends that are reshaping the cybersecurity landscape.

A primary driver is the rising frequency and complexity of cyber threats. Attacks such as ransomware, phishing, and advanced persistent threats (APTs) are becoming more targeted and sophisticated, prompting organizations to adopt specialized hardware solutions for comprehensive network protection.

Another significant factor is increasing digital transformation across sectors. The expansion of cloud computing, IoT, and mobile workforce models has introduced new security vulnerabilities. This shift demands robust appliances that can secure a more dispersed and heterogeneous IT environment.

Regulatory compliance is another vital driver. Governments worldwide are enforcing stringent data protection laws (e.g., GDPR, HIPAA, and CCPA), pushing enterprises to invest in network security appliances that ensure policy enforcement and data integrity.

From a technological standpoint, there is a growing trend towards AI- and ML-powered appliances. These technologies enhance real-time threat detection, reduce false positives, and support automated incident response. Zero Trust Network Architecture (ZTNA) is also gaining traction, leading to increased adoption of network appliances that support micro-segmentation and user-based access control.

Furthermore, the integration of security functionalities into unified platforms is appealing to SMEs seeking cost-effective and simplified security management. Unified Threat Management (UTM) solutions are thus experiencing increased demand.

Lastly, edge security is emerging as a trend, especially with the rise of 5G and edge computing. Appliances are being designed to protect endpoints and data at the network's edge, enabling secure connectivity and processing outside traditional data centers.

Collectively, these drivers and trends indicate a dynamic, innovation-driven market landscape poised for sustained growth.

Regional Analysis

The Network Security Appliance market exhibits varied dynamics across global

regions, influenced by regional cybersecurity awareness, digital infrastructure

maturity, regulatory landscape, and investment trends.

North America leads the global market, driven by the early adoption of advanced technologies, a strong presence of digital enterprises, and stringent data privacy laws. The United States in particular is a major contributor due to the concentration of critical infrastructure, high-value assets, and elevated cybersecurity threats. Continuous government investment in cybersecurity also supports the regional market.

Europe represents the second-largest market, with robust demand from financial services, healthcare, and public sector organizations. The General Data Protection Regulation (GDPR) has heightened awareness and compliance needs, thereby fueling the deployment of network security appliances across the region. Countries such as Germany, the UK, and France are key contributors.

Asia-Pacific is the fastest-growing region due to rapid digitization, expanding IT infrastructure, and increasing incidences of cyberattacks. Countries like China, India, Japan, and South Korea are experiencing heightened demand for network security solutions as businesses and governments digitize operations. Investments in smart cities and Industry 4.0 further boost appliance adoption.

Latin America and the Middle East & Africa (MEA) are witnessing steady growth as cybersecurity awareness improves and digital services become more widespread. Government initiatives to build secure digital economies and increase spending on IT security are expected to enhance market prospects in these regions.

Regional market variations are shaped by differences in threat landscapes, technological maturity, economic development, and regulatory environments. However, the common thread is the growing recognition of network security appliances as essential tools in safeguarding data and ensuring secure digital operations.

Key Players

TXOne Networks, Trend Micro Inc., Palo Alto Networks Inc., NortonLifeLock Inc.,

Juniper Networks Inc., Intel Corporation, Honeywell International Inc., Hewlett

Packard Enterprise Company, Fortinet Inc., Cisco Systems Inc., Check Point

Software Technologies, Jupiner Networks

Contact Us:

Consegic Business intelligence

Email : [email protected]

Sales : [email protected]