Oil Water Separator Market

Introduction

The oil water separator market plays a vital role in supporting industrial sustainability and environmental protection by facilitating the efficient separation of oil from water in diverse industrial and commercial applications. This market is driven by growing awareness of environmental regulations and the need for effective wastewater treatment solutions across industries such as petrochemical, marine, manufacturing, food processing, and transportation. With rising concerns about environmental pollution and stricter discharge limits set by regulatory bodies, the demand for reliable oil water separation technology has increased substantially.

Technological advancements in separation mechanisms, such as gravity-based separators, coalescing plate separators, and hydrocyclone systems, have broadened the applicability and efficiency of these systems. As industries seek cleaner production practices, oil water separators offer a cost-effective and efficient means to comply with regulations while maintaining operational productivity.

The market is witnessing steady growth globally, supported by infrastructure development, industrial expansion, and increased maritime activities. In particular, the use of oil water separators in bilge water treatment, stormwater management, and industrial effluent processing has become more prominent. Investments in R&D and innovation have also fostered the integration of automation and remote monitoring capabilities, aligning with the global push toward smart and sustainable water management solutions.

The future outlook for the oil water separator market remains positive, buoyed by stringent environmental mandates and a growing commitment from industries to achieve zero-liquid discharge and lower carbon footprints. As regulatory frameworks continue to evolve, the market is expected to see a shift toward more advanced, compact, and energy-efficient systems, enabling both large-scale facilities and small operators to meet compliance requirements and sustainability goals effectively.

Definition

An oil water separator is a mechanical device designed to separate oil and other hydrocarbons from water, thereby reducing pollutants before wastewater is released into the environment or reused in various applications. These systems are commonly used in industries that generate oily wastewater, such as manufacturing, automotive, petrochemicals, marine, and food processing. The primary function of oil water separators is to prevent environmental contamination and ensure that discharged water meets regulatory standards.

The principle of separation is based on the difference in specific gravity between oil and water. Since oil is less dense than water, it rises to the surface, where it can be collected or skimmed off, while cleaner water exits the system. Various types of oil water separators are available, including gravity-based separators, coalescing plate separators, centrifugal separators, and membrane-based systems, each suited to different applications and oil concentrations.

Gravity separators utilize simple buoyancy principles and are suitable for free-floating oil, while coalescing plate separators improve efficiency by using inclined plates to encourage oil droplets to merge and rise more quickly. Centrifugal and hydrocyclone separators employ rotational motion to accelerate the separation process, making them ideal for emulsified oils or finer droplets.

The effectiveness of an oil water separator is influenced by factors such as flow rate, oil type, water temperature, and the presence of suspended solids. Advanced systems may include filtration units, automated oil skimmers, and digital monitoring tools to enhance performance and ensure regulatory compliance.

Overall, oil water separators are essential components in industrial wastewater treatment, enabling businesses to manage their waste streams more responsibly. Their role in environmental stewardship and legal compliance has become increasingly important as global focus intensifies on pollution prevention, clean water initiatives, and sustainable industrial practices.

Scope & Overview

The oil water separator market encompasses a wide range of technologies and applications, addressing the global need for efficient separation of oil contaminants from wastewater. These systems are crucial in meeting the rising environmental and operational demands of industries aiming to reduce their ecological footprint while maintaining compliance with increasingly stringent water discharge standards.

The scope of this market extends across several industries, including oil and gas, maritime, food processing, metalworking, and power generation. It covers a diverse portfolio of separator types such as gravity-based separators, coalescing media separators, and pressurized systems designed to handle varying levels of oil content and flow rates. The market also includes aftermarket services, such as maintenance, system upgrades, and retrofitting, offering additional growth opportunities for manufacturers and service providers.

From a technology standpoint, advancements have led to compact, modular designs that can be integrated into both new and existing infrastructure with ease. Modern separators often feature automated operation, real-time monitoring, and minimal maintenance, providing operational efficiency and long-term cost savings. Digital integration, including IoT-enabled systems, further enhances data-driven decision-making and remote diagnostics.

The market is segmented by application, product type, end-user industry, and geography. Applications range from bilge water treatment in ships to runoff water management in municipal systems. Key end-user sectors include manufacturing, marine, and energy industries, each with specific requirements and operational conditions that influence separator design and performance.

As global environmental awareness grows and industrial activities expand in both developed and emerging economies, the oil water separator market is poised for sustained growth. Regulatory trends, environmental policies, and an emphasis on sustainable water management continue to expand the relevance and adoption of these systems, making them an indispensable part of modern industrial ecosystems.

Size

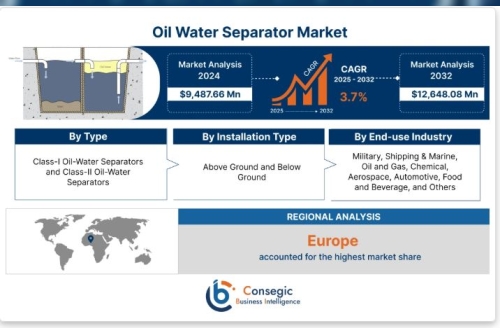

Consegic Business Intelligence analyzes that the oil water separator market size is growing with a CAGR of 3.7% during the forecast period (2025-2032), and the market is projected to be valued at USD 12,648.08 Million by 2032 from USD 9,487.66 Million in 2024.

Segmental Analysis

By Type

Class-I Oil-Water Separators and Class-II Oil-Water Separators

By Installation Type

Above Ground and Below Ground

By End-use Industry

Military, Shipping & Marine, Oil and Gas, Chemical, Aerospace, Automotive, Food and Beverage, and Others

Key Industry Drivers & Trends

The oil water separator market is influenced by several key drivers and emerging trends, underscoring its importance in contemporary industrial and environmental management.

Environmental Regulations:

Stringent global environmental regulations, such as discharge standards set by

EPA, IMO, and other regional bodies, are major market drivers. These policies

compel industries to adopt oil water separators to avoid penalties and ensure

sustainable operations. Compliance has become non-negotiable, pushing adoption

across sectors.

Industrialization and

Urbanization:

Rapid industrial development, particularly in emerging economies, is resulting

in higher wastewater volumes containing oils and greases. This drives the need

for efficient separation systems, especially in manufacturing and energy

sectors. Urban expansion also increases stormwater runoff, another key

application area.

Technological Advancements:

Recent innovations have made oil water separators more compact, efficient, and

cost-effective. Developments in coalescing media, automated sludge removal, and

digital monitoring systems are enhancing performance while reducing maintenance.

Integration with IoT enables real-time analytics and system optimization,

aligning with the shift toward smart water infrastructure.

Focus on Sustainability:

Corporate sustainability initiatives are prompting industries to invest in

cleaner production technologies. Oil water separators contribute to water

reuse, reduced pollution, and better waste management—key components of

sustainable development goals (SDGs).

Growing Marine and Offshore

Activities:

The marine and offshore oil sectors require robust oil water separation

systems, especially for bilge water treatment. With growing maritime traffic

and offshore drilling, demand for marine-grade oil water separators is

increasing.

Emerging Trends:

There is a growing preference for modular and skid-mounted units that are

easier to install and integrate into existing facilities. Customization for

niche applications and increased focus on energy-efficient systems are also

emerging as significant trends.

Together, these drivers and trends form a dynamic landscape that supports ongoing growth and innovation in the oil water separator market.

Regional Analysis

The oil water separator market demonstrates regional diversity in terms of adoption rates, technological advancement, regulatory enforcement, and industrial demand.

North America:

This region maintains a significant share, largely due to rigorous environmental

regulations and strong industrial infrastructure. The United States leads the

adoption of advanced oil water separator technologies, especially in oil &

gas, automotive, and maritime sectors. Investments in upgrading existing

wastewater treatment facilities and innovations in energy-efficient systems

further bolster market growth.

Europe:

Europe’s commitment to environmental protection, backed by regulations such as

the EU Water Framework Directive, drives substantial demand. Countries like

Germany, France, and the UK have well-established industrial bases with a focus

on sustainable waste management. Advanced separator technologies are widely

deployed in manufacturing and maritime industries.

Asia-Pacific:

Asia-Pacific is the fastest-growing market, propelled by rapid

industrialization, urban development, and infrastructure expansion. Countries

such as China, India, and Japan are key contributors. The growing presence of

heavy industries, combined with improving regulatory frameworks and water

scarcity concerns, drives strong market growth in this region.

Latin America:

The Latin American market is expanding gradually, driven by increasing

environmental awareness and industrial development in countries like Brazil and

Mexico. The oil & gas and mining sectors, in particular, present

significant opportunities for oil water separator systems.

Middle East & Africa:

This region holds potential due to its active oil & gas industry and rising

need for water reuse in arid climates. While regulatory enforcement varies,

efforts to diversify economies and improve environmental stewardship are

boosting investments in wastewater treatment infrastructure.

In summary, while North America and Europe remain mature markets driven by regulatory rigor and innovation, Asia-Pacific stands out for its rapid growth trajectory. Meanwhile, emerging regions present future opportunities as industrial and environmental priorities gain momentum.

Key Players

Alfa Laval AB, Andritz AG, Siemens AG, Parker-Hannifin Corporation, Wärtsilä Oyj Abp, Donaldson Company, Inc., Mercer International Inc., ZCL Composites, HSN-Kikai Kogyo, and Highland Tank

Contact Us:

Consegic Business intelligence

Email : [email protected]

Sales : [email protected]