Quantum Dot Display Market Report

Introduction:

The Quantum Dot Display market represents a rapidly emerging segment within the broader display technology industry, offering significant improvements in color accuracy, brightness, and energy efficiency. Quantum dot (QD) technology is gaining traction as a transformative advancement in display panels, especially in television screens, monitors, and mobile devices. This market is being propelled by the increasing consumer demand for high-performance displays that offer lifelike color reproduction and enhanced contrast ratios. With its ability to deliver superior visual experiences compared to traditional LCD and OLED screens, QD technology has positioned itself as a key enabler of next-generation display solutions.

Over the past decade, advancements in nanotechnology have catalyzed the commercial viability of quantum dot displays. These improvements have led to the development of highly efficient and scalable manufacturing processes, making QD displays more accessible for a wider range of applications. As the global electronics industry continues to evolve, the integration of QD technology into consumer electronics, automotive displays, and medical imaging is expected to accelerate.

Moreover, increasing investments in display research, growing adoption of 4K and 8K content, and a shift toward eco-friendly and cadmium-free QD materials are further strengthening the market outlook. Emerging economies in Asia-Pacific, rising disposable incomes, and expanding smart device penetration also contribute to the optimistic growth projections. As consumer preferences shift toward premium visual experiences, the Quantum Dot Display market is poised to become a major driver of innovation and revenue within the broader display industry.

Definition:

Quantum Dot Display refers to a type of flat-panel display technology that utilizes semiconductor nanocrystals known as quantum dots (QDs) to enhance image quality. These nanocrystals are capable of emitting precise wavelengths of light when excited, typically by a blue LED backlight. The emission properties of QDs are tunable based on their size and composition, allowing for highly accurate color reproduction across the visible spectrum. This precise control over light emission enables quantum dot displays to produce richer and more vibrant colors compared to conventional liquid crystal displays (LCDs) and organic light-emitting diode (OLED) technologies.

In a typical QD-enhanced display, a quantum dot enhancement film (QDEF) is placed between the LED backlight and the LCD panel. The QDs absorb the blue light and re-emit red and green light with high efficiency. When combined with the remaining blue light from the LED, the full-color spectrum is generated. This method leads to improved color gamut, increased brightness, and reduced energy consumption.

Quantum dot displays are not standalone panel types like OLED; instead, they are usually an enhancement applied to existing LCDs. However, ongoing research is exploring self-emissive quantum dot displays that do not require backlighting, which may eventually lead to even more advanced and flexible applications. The integration of QD technology into displays represents a blend of nanotechnology and optoelectronics that is reshaping the standards of modern screen performance.

Scope & Overview:

The scope of the Quantum Dot Display market spans multiple end-user industries and a variety of applications that benefit from high-resolution, high-efficiency display technology. This includes consumer electronics such as televisions, smartphones, tablets, and monitors, as well as niche segments like automotive displays, digital signage, and medical imaging. The technology offers a compelling value proposition by combining vivid color output with energy efficiency and longer lifespans, addressing both performance and environmental concerns.

Quantum Dot Displays are positioned as a competitive alternative to OLED displays, especially in large-format and premium display segments. As manufacturing costs continue to decline and production techniques mature, QD technology is increasingly becoming accessible to mid-range product categories as well. The market's evolution is also being influenced by regulatory pressures to reduce cadmium usage, leading to the development of cadmium-free quantum dots and more sustainable materials.

The market is characterized by rapid innovation, with developments in quantum dot integration, self-emissive QD displays, and hybrid QD-OLED solutions. Additionally, consumer preferences for enhanced color reproduction, especially for 4K and 8K ultra-high-definition (UHD) content, are creating demand tailwinds. The growth trajectory is further amplified by strategic collaborations in R&D, infrastructure expansion, and an expanding base of display panel manufacturers integrating QD technologies.

Overall, the Quantum Dot Display market is not only shaping the future of screen technology but also enabling broader advances in entertainment, communication, and visualization, marking it as a key growth engine in the global electronics ecosystem.

Size

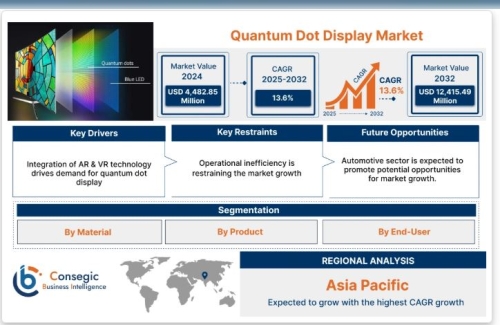

Quantum Dot Display Market size is estimated to reach over USD 12,415.49 Million by 2032 from a value of USD 4,482.85 Million in 2024 and is projected to grow by USD 5,011.74 Million in 2025, growing at a CAGR of 13.6 % from 2025 to 2032.

Segmental Analysis:

By Material

Cadmium Based Quantum Dots Cadmium Free Quantum Dots Water-soluble Quantum Dots OthersBy Product

Tablet PC Monitors TV Display Smartphone OthersBy End-User

Consumer Electronics Healthcare Automotive Others

Key Industry Drivers & Trends:

Several key drivers and trends are shaping the trajectory of the Quantum Dot Display market. One of the foremost drivers is the increasing demand for high-definition and ultra-high-definition content, which necessitates advanced display technologies capable of delivering superior visual experiences. Quantum dots enable wider color gamuts and improved contrast, making them ideal for 4K and 8K screens.

Technological innovation is another major driver. The development of cadmium-free QDs and the emergence of self-emissive QD displays are transforming the landscape by offering sustainable and next-generation solutions. The convergence of QD technology with OLED in hybrid displays further demonstrates the market’s adaptability and innovation potential.

Energy efficiency is a critical trend, especially in portable devices where battery life is paramount. QD displays consume less power compared to OLEDs, offering both performance and efficiency. Environmental regulations are also pushing manufacturers to explore non-toxic materials, further fueling innovation in material sciences.

Consumer preferences are evolving toward displays that offer realistic and immersive visual experiences. This is leading to greater adoption of QD technology in premium product lines across multiple industries. Moreover, rapid urbanization and rising disposable incomes in emerging economies are expanding the addressable market for QD-enhanced devices.

Another trend is the increasing R&D collaboration among universities, startups, and display manufacturers, which is accelerating the commercialization of advanced QD technologies. Overall, the market is poised for robust growth, driven by innovation, consumer demand, and sustainability.

Regional Analysis:

Regionally, the Quantum Dot Display market is most prominently concentrated in the Asia-Pacific region, which holds a dominant share due to its strong electronics manufacturing infrastructure, especially in countries like South Korea, China, and Japan. These nations not only host leading display panel manufacturers but also serve as major export hubs for consumer electronics. Government support for nanotechnology R&D and rapid industrialization further enhance the region’s market leadership.

North America follows closely, benefiting from advanced technological ecosystems, high consumer spending on premium electronics, and strong emphasis on innovation. The region also hosts a number of research institutions and startups working on advanced QD materials and display applications, contributing to a robust innovation pipeline.

Europe is witnessing steady growth in the QD display market, driven by increasing demand for energy-efficient and eco-friendly display technologies. The region’s focus on sustainability has led to rising interest in cadmium-free quantum dots, aligning with EU environmental directives. European consumers’ inclination toward high-end display solutions in both professional and personal settings supports market expansion.

Latin America, the Middle East, and Africa are still nascent markets for QD displays but are gradually gaining traction as the penetration of smart devices increases. Rising urbanization, expanding middle-class populations, and growing access to digital content in these regions are expected to create new opportunities for market growth.

Overall, regional dynamics are shaped by varying levels of technological readiness, consumer demand, and industrial support, with Asia-Pacific remaining the growth epicenter.

Key Players:

Suzhou Xingshuo Nanotech Co. Ltd. (China)

Avantama AG (Switzerland)

SAMSUNG DISPLAY (South Korea)

Nanoco Group plc (UK)

Quantum Materials Corporation (US)

Sheoi Electronic Materials, Inc. (US)

LG Electronics. (South Korea)

Sony Corporation (Japan)

QD Vision Inc. (US)

3M Company (US)

Contact Us:

Consegic Business intelligence

Email : [email protected]

Sales : [email protected]