Semiconductor Inspection System Market Report

Introduction:

The semiconductor inspection system

market plays a pivotal role in ensuring quality, reliability,

and performance in the rapidly evolving semiconductor industry. These systems

are essential for identifying defects and anomalies during the semiconductor

manufacturing process, thus maintaining high yield rates and reducing costly

failures. With the miniaturization of semiconductor devices and the increasing

complexity of integrated circuits, the demand for highly accurate and sensitive

inspection solutions has surged. These systems are integrated across various

production stages, including wafer fabrication, packaging, and final testing,

to detect microscopic defects and contaminants.

Growing adoption of advanced nodes such as 5nm and 3nm technologies in logic and memory chips has significantly elevated the need for precision inspection systems. The market has seen a consistent rise in investment in research and development, fueled by global trends like 5G deployment, AI computing, and electric vehicles, all of which require high-performance semiconductor components. As a result, the semiconductor inspection system market is projected to witness robust growth across foundries, integrated device manufacturers (IDMs), and outsourced semiconductor assembly and testing (OSAT) companies.

The competitive landscape is also shaped by increasing automation, machine learning integration, and demand for high-throughput inspection tools. Additionally, geopolitical factors and supply chain challenges are influencing market strategies and regional investments. As global electronics demand continues to rise, especially in consumer devices and automotive electronics, the semiconductor inspection system market is expected to remain a critical enabler of technology innovation and quality assurance.

Definition:

Semiconductor inspection systems

are specialized tools used to detect defects, particles, pattern deviations,

and process abnormalities in semiconductor wafers and packages during the

manufacturing lifecycle. These systems play a critical role in identifying

issues that may affect the functionality, yield, or performance of

semiconductor devices. Inspection systems operate through optical, electron

beam, and other imaging technologies to scrutinize the surface and sub-surface

structures of wafers with high resolution and sensitivity.

There are two main categories of inspection: patterned and unpatterned. Patterned wafer inspection involves examining wafers post-lithography to detect misalignments, scratches, or contaminations. Unpatterned inspection, on the other hand, is used early in the process to identify particles and surface roughness. Modern inspection systems may employ advanced features like deep learning algorithms and defect classification to differentiate between critical and non-critical defects.

The systems can be classified based on their application stage such as front-end (wafer fabrication) or back-end (assembly and packaging). They may also vary by inspection type including macro, micro, and nano-inspection, depending on the resolution and magnification required. By incorporating various sensing and imaging techniques, these systems ensure early fault detection, reduce yield loss, and optimize process control.

Overall, semiconductor inspection systems are indispensable in upholding the standards of increasingly complex chip designs. With technological advancements driving smaller geometries and higher density circuits, inspection solutions have evolved to meet stringent detection limits and faster throughput requirements. They act as a quality gate throughout the semiconductor production line, making them essential to the efficiency and competitiveness of semiconductor manufacturers.

Scope & Overview:

The semiconductor inspection system market encompasses a wide array of

technologies and solutions used throughout the semiconductor production chain

to ensure product quality and manufacturing efficiency. This market includes both

equipment and software used for optical inspection, electron beam inspection,

metrology, and defect analysis in both front-end and back-end semiconductor

processes.

The market scope spans multiple industries such as consumer electronics, automotive, telecommunications, and industrial automation, where high-performance semiconductor devices are fundamental. Within these sectors, inspection systems are applied to detect faults in wafers, photomasks, interconnects, and encapsulation processes. The increasing demand for advanced process nodes, higher transistor densities, and 3D architectures has expanded the need for high-resolution and fast-throughput inspection solutions.

From a value chain perspective, the market includes equipment manufacturers, inspection software developers, system integrators, and end-users like semiconductor foundries and test houses. Technological innovations like AI-powered inspection, real-time defect classification, and nanoscale imaging are enhancing inspection accuracy and speed, thus improving overall production economics.

The market is also influenced by factors such as R&D investment, regulatory compliance, and cross-border trade dynamics. Emerging regions are increasingly investing in domestic semiconductor manufacturing, thereby broadening the geographic scope of inspection system demand. Moreover, the push toward Industry 4.0 and smart manufacturing is fostering integration of inspection systems with automated production lines and data analytics platforms.

Overall, the semiconductor inspection system market is evolving rapidly with growing emphasis on yield enhancement, cost efficiency, and technological scalability. It is well-positioned to expand in line with global semiconductor demand, offering diverse opportunities across applications, geographies, and technology types.

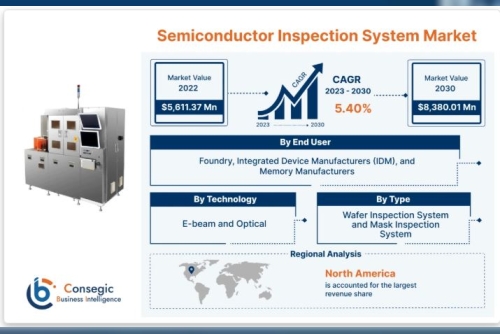

Size

Semiconductor Inspection System Market size is estimated to reach over USD 8,380.01 Million by 2030 from a value of USD 5,611.37 Million in 2022, growing at a CAGR of 5.40% from 2023 to 2030.

Segmental Analysis:

By Type

Wafer Inspection System and Mask Inspection System

By Technology

E-beam and Optical

By End User

Foundry, Integrated Device Manufacturers (IDM), and Memory Manufacturers

Key Industry Drivers &

Trends:

Several key drivers and emerging trends are shaping the growth and innovation

in the semiconductor inspection system market. Chief among them is the

relentless pursuit of smaller and more efficient chips, driving the need for

advanced inspection technologies that can detect minute defects and structural

anomalies at nanoscale levels.

Technology Scaling: As chip architectures evolve toward smaller nodes (5nm, 3nm, and beyond), traditional inspection techniques face limitations in resolution and throughput. This has led to rising demand for advanced inspection systems using electron beam and AI-powered analytics capable of processing vast data with precision.

Rise in Complex Packaging: Advanced packaging technologies such as 2.5D and 3D ICs require new inspection solutions to manage increased interconnect density and new materials. The inspection of through-silicon vias (TSVs) and microbumps has become a crucial part of maintaining yield in heterogeneous integration.

Growing Semiconductor Demand: The proliferation of 5G, IoT, electric vehicles, and artificial intelligence is fueling semiconductor demand, pushing manufacturers to enhance their quality assurance processes. This translates directly into higher demand for inspection systems that ensure defect-free high-performance chips.

Automation and Industry 4.0 Integration: Smart manufacturing and automation trends are integrating inspection systems with MES (Manufacturing Execution Systems) and big data analytics platforms. This enhances defect traceability and predictive maintenance, driving process efficiency.

Supply Chain Localization: As nations invest in domestic semiconductor manufacturing to secure supply chains, inspection system vendors are gaining new opportunities in previously underserved regions.

In summary, continuous technology scaling, complex chip designs, and evolving end-user demands are reinforcing the central role of inspection systems. These trends ensure that inspection technology remains at the forefront of semiconductor manufacturing innovation.

Regional Analysis:

The semiconductor inspection system market exhibits significant regional

variation, with major contributions coming from Asia-Pacific, North America,

Europe, and emerging economies in the Middle East and Latin America.

Asia-Pacific holds the dominant position in the market, driven by the presence of leading foundries and integrated device manufacturers. Countries such as Taiwan, South Korea, China, and Japan invest heavily in semiconductor fabrication infrastructure, thereby generating strong demand for inspection systems. China’s push for semiconductor self-sufficiency also contributes significantly to regional growth, leading to increased domestic production and technology adoption.

North America remains a critical region due to its focus on advanced R&D, presence of major semiconductor equipment manufacturers, and investment in next-generation fabrication technologies. The U.S. government’s support for domestic semiconductor initiatives is expected to stimulate demand for sophisticated inspection tools, especially for cutting-edge nodes.

Europe shows steady growth, particularly in the automotive semiconductor segment and industrial electronics. Germany and the Netherlands are notable contributors, emphasizing innovation and precision in semiconductor equipment and materials. The region’s focus on energy efficiency and industrial automation also supports semiconductor inspection demand.

Emerging Regions such as Southeast Asia and India are gradually expanding their footprint in semiconductor packaging and testing. Government-led initiatives and partnerships with global technology providers are paving the way for increased adoption of inspection systems in these regions.

Overall, regional market dynamics are influenced by investment in semiconductor fabrication, technological readiness, and supply chain strategies. As global demand continues to rise, regional markets are expected to expand both in terms of capacity and technological capability, offering growth opportunities across the board.

Key Players:

ViSCO Technologies USA, Inc., TAKANO CO., LTD., UENO SEIKI CO., LTD., Nikon

Metrology NV., Toray Engineering (TASMIT, Inc.), Onto Innovation, Inc., C&D

Semiconductor Services Inc., Lasertec Corporation, KLA Corporation, Applied

Materials Inc., Hitachi Group, ASML Holding N.V., and JEOL Ltd.

Contact Us:

Consegic Business intelligence

Email : [email protected]

Sales : [email protected]

Furnished 1-Bhk Apt Rent in Bashundhara R/A,Dhaka

Furnished 1-Bhk Apt Rent in Bashundhara R/A,Dhaka