The global cell expansion market size was valued at USD 17.75 billion in 2022 and is expected to register a compound annual growth rate (CAGR) of 12.85% from 2023 to 2030. The increase in the usage of automated solutions in cell expansion applications is one of the primary market drivers. Automated systems minimize the manpower and costs incurred during the production of Cell Therapy Products (CTP), gene therapies, and other biologics, leading to robust and reliable processes.

Key players engaged in CTP development are expanding their product lines to address the significant rise in global demand for these therapy products. For instance, in January 2021, Thermo Fisher Scientific introduced the Gibco CTS OpTmizer Pro Serum Free Media platform for developing and expanding human T lymphocytes for cell therapy developers using allogeneic workflows. This platform targets donor cell metabolism, making it suitable for allogeneic, off-the-shelf cell therapies.

The paradigm shift toward Single-Use Systems (SUS) offers substantial production advantages in CTP manufacturing. SUS eliminates concerns of cross-contamination and culture contamination caused due to inappropriate sterilization. SUS also allows the production of CTP with high cell densities and offers cost savings in the long run. Thus, a rise in the adoption of SUS surges the development of CTP, which boosts market growth.

Gather more insights about the market drivers, restrains and growth of the Global Cell Expansion Market

Global Cell Expansion Market Report Segmentation:

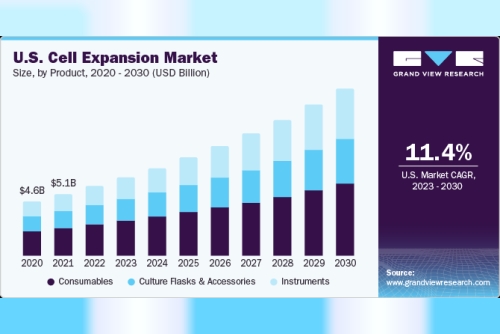

Product Insights

Consumables led the product segment in 2022 and accounted for 45.7% of the overall market share. The segment is furthermore estimated to retain its dominant position throughout the forecast years. The availability of a wide range of commercial media and reagent products that are dedicated to specific types of cells contributes to the large revenue share of this segment. In addition, these products are convenient, ready to use, and are also available as serum-free formulations.

Cell Type Insights

The mammalian cells segment held the highest revenue share in 2022 and is expected to remain dominant during the forecast period, as these culture systems are highly preferred in the production of complex protein therapeutics. This is because these systems are pharmacokinetically and functionally relevant to post-translational modifications in humans. Therefore, most of the biopharmaceuticals, including monoclonal antibodies, specific interferons, thrombolytics, and various therapeutic enzymes, are produced using these culture systems.

End-use Insights

The biotechnology & biopharmaceutical companies segment held the largest share of 46.3% in 2022 and is poised to expand further at a significant growth rate. The broadening horizon of cell-based therapeutics in the healthcare industry is one of the major factors contributing to the large share of biopharmaceutical companies. For instance, cellular-based therapies have gained immense popularity in regenerative medicine, with constant improvements in injectable cell delivery systems for various clinical applications.

Application Insights

The biopharmaceutical segment captured the largest revenue share owing to an increase in the approval rate of biopharmaceutical products in the past few years. The entry of new biopharmaceutical companies and the proliferation of bioprocessing technologies further drive the development of biopharmaceuticals, which, in turn, boosts the expansion procedures conducted during bio-production.

Browse through Grand View Research's Medical Devices Industry Research Reports.

Medical Device Analytical Testing Outsourcing Market: The global medical device analytical testing outsourcing market size was valued at USD 5.66 billion in 2022 and is anticipated to grow at a compound annual growth rate (CAGR) of 8.2% from 2023 to 2030.Resectoscope Devices Market: The global resectoscope devices market size was estimated at USD 414.62 million in 2024 and is projected to grow at a CAGR of 5.36% from 2025 to 2030.Regional Insights

North America accounted for the largest revenue share of 39.0% in 2022. The region is anticipated to retain its leading position in the coming years due to a rise in funding initiatives by government agencies, which has accelerated the manufacturing of stem cells and the development of regenerative medicines and cellular therapy products. This, in turn, drives the demand for cell expansion platforms in this region.

Key Companies & Market Share Insights

Key market participants are undertaking several initiatives to expand their market presence and maintain a competitive edge. Moreover, they are involved in collaborations & partnership models, product development, agreements, and business expansion strategies in untapped regions.

For instance, in April 2022, STEMCELL Technologies Canada and Applied Cells Inc. joined forces to develop a modern way to separate cells, through the combination of the MARS platform of Applied Cells with STEMCELL's EasySep kits to make isolating cells from different samples easier and more automatic. These samples can be from whole blood, bone marrow, apheresis products, and tissue. The collaboration aims to improve the process of isolation of cells for research and medical purposes, making it more efficient and effective.

In another development, in May 2023, a research agreement was signed by panCELLa and BioCentriq to study stem cell-derived Natural Killer cell expansion technology. The agreement aims to evaluate panCELLa’s feeder cells, which are genetically engineered, to positively impact the expansion rate, total yield, and potency of manufactured NK cells.

Key Cell Expansion Companies:

Thermo Fisher Scientific, Inc.Corning IncorporatedMerck KGaAMiltenyi BiotecBD (Becton, Dickinson and Company)Terumo BCT, Inc.Sartorius AGTakara Bio Inc.TRINOVA BIOCHEM GmbHupcyte technologies GmbHOrder a free sample PDF of the Cell Expansion Market Intelligence Study, published by Grand View Research.