The global clinical workflow solutions market size is estimated to reach USD 24.37 billion by 2030, growing at a CAGR of 12.4% from 2023 to 2030, according to a new report by Grand View Research, Inc. The need for clinical process automation is expanding, especially in developed countries like the U.S., and rising initiatives from public and commercial organizations are changing the healthcare sector. The need for scalable healthcare systems has been further spurred by the requirement to give clinicians remote access to data insights. For instance, according to a survey conducted by OmniLife Health in March 2023, over 30% of the U.S. hospitals, health systems, and transplant centers have already implemented Clinical Workflow Automation (CWA), which is expected to rise to 61% by 2024.

In addition, 48% of companies utilizing CWA want to deploy it in more clinical settings by 2023. Given that some respondents wrongly assume their current EHR vendor or simple software programs may deliver CWA functions, the expansion of CWA is anticipated to continue as there is still substantial scope for expanded adoption. The adoption rate is anticipated to increase as public knowledge and comprehension of CWA grow.

Healthcare providers have faced substantial hurdles during the COVID-19 epidemic, highlighting the need for remote access to data insights and effective clinical procedures. As a result, businesses are expanding their markets and engaging in more acquisitions to diversify and synchronize their product portfolios. For instance, in December 2021, Fortive announced to pay USD 1.4 billion to acquire Provation, a provider of clinical workflow solutions. This tactical move strengthens Fortive's position in crucial workflow solutions for hospitals and ambulatory surgical centers (ASCs) and aligns with the company's Advanced Healthcare Solutions (AHS) segment.

Gather more insights about the market drivers, restrains and growth of the Global Clinical Workflow Solutions Market

To maintain a strong competitive advantage, market participants are actively investing in creating and introducing innovative products. For instance, in February 2023, bioMérieux launched MAESTRIA, a cutting-edge middleware solution for the clinical microbiology laboratory. As a centralized software solution, MAESTRIA streamlines operations and improves operational efficiency by managing the workflow of everyday tasks. This strategic decision demonstrates the market's competitors' dedication to providing innovative, all-inclusive solutions to satisfy clinical laboratories' changing demands.

Furthermore, the market is also expanding due to the rising demand for AI-assisted technology, which is renowned for minimizing errors and assisting with clinical decision-making. This tendency will persist with the launch and adoption of additional AI-assisted technologies. For instance, in October 2022, ConcertAI's TeraRecon unveiled TeraRecon Neuro, an AI-assisted clinical workflow solution created to solve time issues in neurovascular crises for the whole care team.

Clinical Workflow Solutions Market Report Highlights

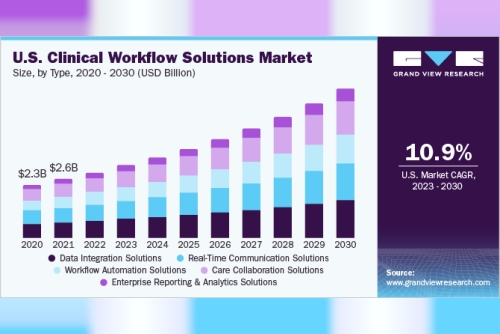

Based on type, the data integration solutions category dominated the market with a share of 26.53% in 2022. Owing to the increasing amounts of data and the demand for integrated solutions to lower escalating costs, healthcare providers have chosen data integration technologiesBased on end-use, the hospitals segment led the market with a revenue share of 44.9% in 2022. This is attributed to the extensive use of clinical workflow solutions in hospitals and the increased number of healthcare institutions requiring efficient data management and privacy protectionThe North America region dominated the market with a revenue share of 41.84% in 2022. The increasing R&D activities and hospital patient admission lead to a high volume of data generated and increasing government initiatives regarding the effective usage of interoperability provide the market with the largest revenue contributionSeveral companies are actively collaborating to promote innovation in workflow solutions. For instance, Innovaccer and Roche announced a collaboration to provide clinical decision support and workflow solutions in September 2021. Such collaborations are critical in driving the market acceptance and development of efficient workflow solutionsList of Key Players in the Clinical Workflow Solutions Market

Allscripts Healthcare Solutions, Inc.Cerner CorporationNXGN Management, LLCMcKesson CorporationKoninklijke Philips N.V.Hill-Rom Services Inc.CiscoGeneral ElectricStanly HealthcareVocera CommunicationsASCOMathenahealth, Inc.Order a free sample PDF of the Clinical Workflow Solutions Market Intelligence Study, published by Grand View Research.