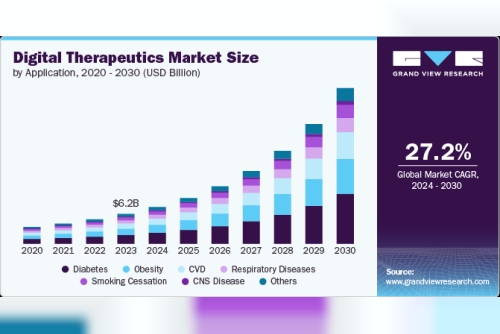

The global digital therapeutics market was valued at USD 6.2 billion in 2023 and is projected to expand at a compound annual growth rate (CAGR) of 27.2% from 2024 to 2030. This robust growth is primarily fueled by the cost-efficiency of digital health technologies for both providers and patients, along with increasing smartphone adoption in both developed and emerging economies. A growing demand for patient-centric care and integrated healthcare systems further contributes to market expansion. Additional drivers include favorable reimbursement policies, the COVID-19 pandemic, a rise in chronic disease prevalence, and widespread adoption of digital health solutions.

Global internet expansion has also positively influenced market dynamics. According to the GSM Association’s Mobile Economy 2024 report, approximately 5.6 billion people subscribed to mobile services in 2023, with the number expected to grow to 6.3 billion by 2030. Furthermore, smartphone penetration, which stood at 76% in 2022, is forecasted to reach 92% by 2030, according to the Mobile Economy 2023 report. This surge is anticipated to elevate both awareness and use of intelligent health monitoring tools.

Improvements in network infrastructure and broader coverage are expected to further stimulate demand for digital therapeutics. Mobile network operators increasingly view digital health as a valuable investment opportunity, largely due to rising smartphone usage. The GSMA's 2023 report predicts that global 5G penetration will reach 54% by 2030. Enhanced bandwidth and reduced latency offered by 5G are expected to significantly improve the quality of virtual healthcare interactions, enabling high-resolution image and video sharing. This will lessen the need for in-person visits and improve access for patients in remote or underserved areas.

The COVID-19 pandemic played a pivotal role in accelerating digital therapeutics adoption by enabling greater regulatory flexibility and expanding patient access to digital health tools. For example, FDA guidelines released in April 2020 permitted the use and distribution of digital therapeutics for psychiatric conditions during the public health emergency, without full regulatory compliance—as long as safety was ensured.

The rising prevalence of chronic diseases is another key market driver. According to the CDC’s National Center for Chronic Disease Prevention and Health Promotion, 6 in 10 American adults live with at least one chronic disease, and 4 in 10 suffer from two or more. In response, major initiatives are being launched. For instance, in January 2024, Amazon Health introduced its Health Condition Programs to support chronic disease management through digital solutions aimed at conditions like diabetes and hypertension. Chronic illnesses such as cardiovascular disease, diabetes, Alzheimer’s, cancer, lung disease, and kidney disease continue to be leading causes of death and disability in the U.S.

The regulatory landscape for digital therapeutics is becoming increasingly favorable, encouraging greater investment and innovation. There is also a growing shift toward value-based care models, which prioritize patient outcomes and cost efficiency over service volume. Digital therapeutics are well-aligned with this approach, offering measurable improvements in patient health and reduced healthcare expenses.

Recent policy developments further strengthen the digital therapeutics ecosystem. The FDA’s creation of the Digital Health Center of Excellence and the introduction of reimbursement codes for remote therapeutic monitoring (RTM) have paved the way for broader adoption. These RTM codes—98975, 98976, 98977, 98980, and 98981—cover device setup, patient education, and clinical time dedicated to RTM services, supporting remote and chronic care workflows.

Get a preview of the latest developments in the Global Digital Therapeutics Market! Download your FREE sample PDF today and explore key data and trends

Regional InsightsNorth America held the largest revenue share in 2023, accounting for 40.43% of the global market. The region is expected to maintain strong growth momentum through the forecast period, driven by high digital health adoption, favorable reimbursement environments, and efforts to improve quality of life via better diagnostics and monitoring. Factors such as increasing smartphone usage, network infrastructure enhancements, a growing elderly population, and the rising burden of chronic illnesses all contribute to the region’s digital therapeutics expansion.

Leading Companies in the Digital Therapeutics MarketThe following companies represent the major players in the global digital therapeutics market and collectively shape industry trends:

OMADA HEALTH, INC.

Welldoc, Inc.

2Morrow, Inc

Livongo Health, Inc. (Teladoc Health, Inc.)

Propeller Health (ResMed)

Fitbit LLC

Mango Health

CANARY HEALTH

Noom, Inc.

Pear Therapeutics, Inc.

Akili Interactive Labs, Inc.

HYGIEIA

DarioHealth Corp.

BigHealth

GAIA AG

Limbix Health, Inc.

Gather more insights about the market drivers, restrains and growth of the Digital Therapeutics Market