The global positioning systems (GPS) market was valued at USD 94.25 billion in 2022 and is projected to grow at a compound annual growth rate (CAGR) of 16.1% from 2023 to 2030. This growth is largely driven by the increasing adoption of smartphones and the rising number of GPS-equipped vehicles. In addition, expanding social media usage in developing countries and an uptick in mergers and acquisitions among component manufacturers and system integrators are expected to further propel market expansion during the forecast period.

Over time, GPS has evolved into a widely used tool for navigation. Recent years have seen a surge in the use of GPS-enabled smartphones, fueled by the widespread adoption of e-hailing services worldwide. These systems provide various benefits in road-based applications, such as improved travel convenience and precise tracking of assets and operations. The growing implementation of smart mobility solutions—including navigation, fleet management, satellite-based traffic monitoring, and more—is also expected to drive market growth through 2030.

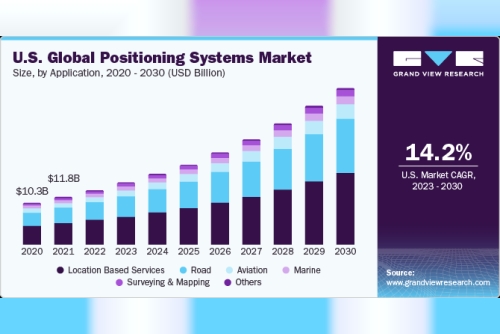

Application Insights

GPS technology serves a wide range of applications, including road transportation, aviation, marine navigation, surveying and mapping, and location-based services. In 2022, the location-based services segment held the largest market share at 42.9%. This dominance can be attributed to changing consumer preferences, particularly the growing use of e-commerce and e-hailing platforms.

Deployment Insights

In terms of deployment, consumer devices accounted for the largest revenue share—45.2% in 2022—driven by the widespread use of smartphones, tablets, and PCs. GPS is commonly embedded in these devices and is also utilized in other products such as automotive telematics systems, portable navigators, and standalone tracking devices.

Regional Insights

The report evaluates key regions including North America, Europe, Asia Pacific, South America, and the Middle East and Africa (MEA). North America remains a major growth region, underpinned by substantial government defense spending—about 4.0% of GDP annually—and high smartphone penetration. The increasing demand for location-based services, spurred by rising smartphone usage, is expected to support robust market growth in this region over the forecast period.

Get a preview of the latest developments in the Global Positioning Systems Market! Download your FREE sample PDF today and explore key data and trends

Key Companies & Market Share Insights

Leading companies in the GPS industry continue to pursue both organic and inorganic strategies to strengthen their market positions. These strategies include product launches, acquisitions, and partnerships aimed at expanding global presence. For example, in April 2023, Syntony GNSS—a key provider of Software-Defined Radio (SDR) Positioning, Navigation, and Timing (PNT) solutions—announced the integration of Xona Space Systems' Low Earth Orbit (LEO) PNT constellation into its GNSS receivers and simulators. This integration enhances signal strength, security, and accuracy, providing improved resistance to spoofing, jamming, and multipath interference in challenging RF environments. This collaboration highlights efforts to develop resilient and advanced PNT technologies.

Key Global Positioning Systems Companies:

Hexagon AB

Qualcomm Technologies, Inc.

Broadcom

Trimble Inc.

MiTAC Holdings Corp

TomTom International BV

Collins Aerospace

Texas Instruments Incorporated

Garmin Ltd.

Gather more insights about the market drivers, restrains and growth of the Positioning Systems Market