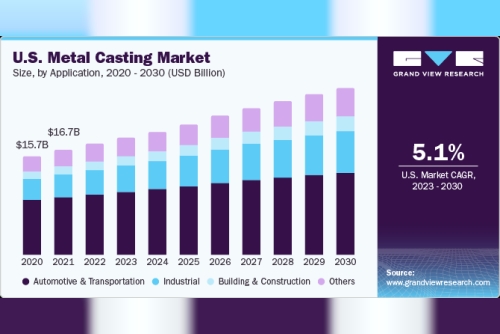

The global metal casting market was valued at USD 136.71 billion in 2022 and is projected to grow at a compound annual growth rate (CAGR) of 5.5% from 2023 to 2030. The growth is primarily driven by increasing demand from the automotive sector, which relies on casting for producing complex and large-size parts. Metal casting, a prominent manufacturing method, involves pouring molten metal into molds to form desired shapes. The demand for lightweight vehicles, driven by stringent regulations on pollution and energy efficiency, is further boosting the market.

The lightweight properties and aesthetic appeal of aluminum castings are also fueling demand in the construction sector. Aluminum castings are widely used in construction equipment, heavy vehicles, curtain walling, and other building components. Furthermore, the recyclability of aluminum supports environmentally sustainable practices, as deconstruction of buildings increasingly replaces demolition. This shift reduces the environmental impact of construction.

Cast iron, an alloy composed of metals like silicon, carbon, and manganese, is in demand due to its applications in cookware, engines, pipes, and automotive parts. Grey iron, in particular, is used for housing, engine blocks, and cylinder heads due to its stiffness, thermal conductivity, and wear resistance.

Gather more insights about the market drivers, restrains and growth of the Global Metal Casting Market

The Asia Pacific region is expected to be a major growth driver due to rising product demand across various industries. The use of aluminum and stainless-steel cast products in healthcare and telecom further propels market growth. The region's building and construction sector, particularly in countries like China, India, and Indonesia, plays a crucial role in driving demand for cast products. For example, Malaysia's construction sector grew by 4.4% in real terms in 2018, while Indonesia's building sector experienced growth of 7-8%. Government incentives, such as Indonesia's relaxed mortgage rules, support this growth, contributing to the metal casting market's expansion.

In the automotive sector, the increasing adoption of lightweight aluminum is a significant growth driver. Regulatory targets like the Corporate Average Fuel Economy (CAFE) standards have prompted vehicle manufacturers to use aluminum to enhance fuel efficiency and reduce emissions. Technological advancements in the automotive industry, coupled with strong demand in markets such as China, South Korea, and India, further boost aluminum casting demand. For instance, the average aluminum content in lightweight vehicles in the U.S. rose by over 4% between 2017 and 2018.

Regional Insights:

Asia Pacific Metal Casting Market Trends

In 2022, Asia Pacific dominated the market, holding a 55.4% revenue share. Low labor costs and favorable policies make the region attractive for manufacturers. China, in particular, has emerged as a hub for cost-effective and high-tech manufacturing, bolstered by skilled labor and supportive government initiatives. The automobile sector's rapid growth in the region is expected to sustain market expansion.

Europe Metal Casting Market Trends

In Europe, the metal casting market is expected to grow at a moderate CAGR of 4.8% between 2023 and 2030. The region's 4,500 metal casting firms, mostly small businesses, and a strong automotive industry, particularly in Germany, Italy, and France, will likely drive demand for aluminum-based casting solutions.

Browse through Grand View Research's Advanced Interior Materials Industry Research Reports.

Wood And Laminate Flooring Market: The global wood and laminate flooring market size was estimated at USD 58.96 billion in 2024 and is projected to grow at a CAGR of 5.5% from 2025 to 2030.Building And Construction Sheets Market: The global building and construction sheets market size was estimated at USD 166.92 billion in 2024 and is expected to grow at CAGR of 5.2% from 2025 to 2030.Key Companies & Market Dynamics

The global metal casting market is fragmented, with numerous small and medium enterprises (SMEs) contributing to an unorganized structure. Key players are focused on expanding production capacities and addressing challenges such as underutilization, resource optimization, high energy consumption, and stringent compliance norms. The increasing use of aluminum in vehicles presents significant opportunities, encouraging companies to develop new alloys and materials.

Key Metal Casting Companies:

POSCODynacastArconicRyobi LimitedEndurance Technologies LimitedAlcast TechnologiesUNI AbexMES, Inc.CALMETHitachi, Ltd.Order a free sample PDF of the Metal Casting Market Intelligence Study, published by Grand View Research.

Redirect emoji domains to your website to increase traffic and domain rating

Redirect emoji domains to your website to increase traffic and domain rating