The global multi-vendor support services market size was estimated at USD 54.14 billion in 2023 and is anticipated to grow at a CAGR of 4.5% from 2024 to 2030. The multi-vendor support services market is primarily driven by the increasing complexity and heterogeneity of IT environments in modern organizations. As businesses adopt a diverse array of hardware, software, and networking solutions from various manufacturers, the need for integrated support services that can manage and optimize these multi-vendor ecosystems becomes critical.

In addition, the demand for cost-effective and streamlined operations compels organizations to seek unified support services, reducing the logistical burden of coordinating with multiple vendors. The rapid pace of technological advancements and the proliferation of cloud-based solutions further amplify the necessity for comprehensive multi-vendor support, ensuring uninterrupted performance and facilitating seamless integration and innovation across diverse IT landscapes.

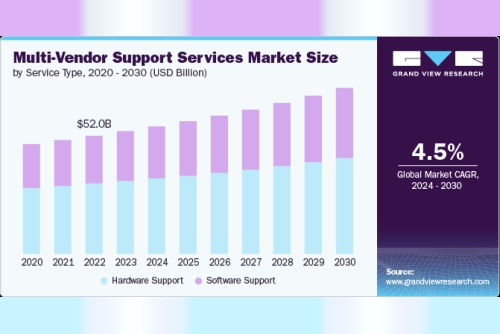

Gather more insights about the market drivers, restrains and growth of the Global Multi-Vendor Support Services Market

The multi-vendor support services market encompasses specialized companies' services to manage, maintain, and optimize equipment and software from multiple manufacturers. These services include technical support, repair, maintenance, and IT infrastructure management to ensure seamless interoperability and peak performance across diverse technological ecosystems. Businesses leverage multi-vendor support services to streamline operations, reduce downtime, and minimize the complexity of dealing with multiple vendors, enhancing efficiency and cost-effectiveness. This market is driven by the growing complexity of IT environments and the need for comprehensive, integrated solutions that can adapt to rapidly evolving technological landscapes.

The increasing complexity and heterogeneity of IT environments in modern organizations significantly drive the multi-vendor support services market by necessitating comprehensive management solutions that can handle diverse technologies. As businesses integrate various hardware, software, and networking components from multiple vendors to meet specific operational needs, the intricacy of maintaining and optimizing these disparate systems grows.

This complexity results in heightened challenges for internal IT departments, which may need more specialized knowledge to manage all aspects effectively. Consequently, organizations turn to multi-vendor support services to ensure seamless interoperability, reduce the risk of downtime, and streamline troubleshooting processes. These services offer the expertise and unified approach needed to navigate the multifaceted IT landscapes, enhancing operational efficiency and enabling businesses to focus on core activities while ensuring their technological infrastructure remains robust and reliable.

Regional Insights

North America held the major share of over 41% of the multi-vendor support services market in 2023. The multi-vendor support services market in North America is experiencing significant growth, driven by the increasing complexity of IT infrastructures and the need for streamlined operations. Businesses seek comprehensive solutions from various manufacturers to manage diverse systems and equipment. The U.S. is at the forefront of this trend, strongly emphasizing reducing downtime and enhancing system efficiency. The presence of significant technology hubs and a high adoption rate of advanced IT solutions contribute to the robust demand in this region.

Key Multi-Vendor Support Services Company Insights

Key players operating in the network emulator market include Atos SE, Cisco Systems, Inc., Dell Inc., DXC Technology Company, Fujitsu, Hewlett Packard Enterprise Development LP, Hitachi, Ltd., International Business Machines Corporation, Oracle, and Unisys. The companies are focusing on various strategic initiatives, including new product development, partnerships & collaborations, and agreements to gain a competitive advantage over their rivals. The following are some instances of such initiatives.

In June 2024, Atos announced the launch of its Atos Virtual Infrastructure Proficiency (VIP) Advisory services. This innovative technology consulting offering is designed to assist companies in evaluating their current virtual infrastructure and defining a strategic roadmap to achieve their future vision. Whether clients choose to retain their existing solutions, remain on-premises, or migrate to a different cloud provider, these pioneering virtual infrastructure consulting services will offer guidance on optimizing virtual infrastructure costs and enhancing security, while embracing new technology trends and advancing corporate sustainability objectives. This offering is offered in the U.S., Central Europe, the UK, Benelux, France.In May 2024, DXC Technology Company, announced its new DXC Fast RISE with SAP service. This offering enables customers to significantly expedite their S/4HANA projects, allowing them to realize the extensive benefits more swiftly than ever before. With DXC Fast RISE with SAP, customers can complete SAP deployments in under twelve months, thereby achieving a quicker time-to-value. The service is designed to be scalable, enabling clients to adapt and expand with minimal disruption. By streamlining the execution process, businesses can reduce their aggregate cost of ownership correlated with SAP adoption.Key Multi-Vendor Support Services Companies:

The following are the leading companies in the multi-vendor support services market. These companies collectively hold the largest market share and dictate industry trends.

Atos SECisco Systems, Inc.Dell Inc.DXC Technology CompanyFujitsuHewlett Packard Enterprise Development LPHitachi, Ltd.International Business Machines CorporationOracleUnisysOrder a free sample PDF of the Multi-Vendor Support Services Market Intelligence Study, published by Grand View Research.