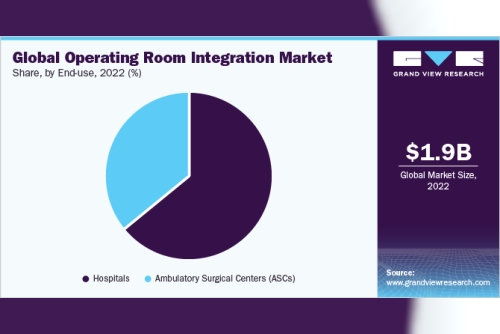

The global operating room integration market size was estimated at USD 1.86 billion in 2022 and is expected to grow at a compound annual growth rate (CAGR) of 11.4% from 2023 to 2030. Increasing demand for technologically advanced Applications, a growing number of surgical procedures, congestion in Operating Rooms (OR), patient safety concerns in OR coupled with the surge in preference for Minimally Invasive Surgeries (MIS) are major factors primarily fueling the market growth. A decrease in the number of surgical procedures led to a decline in demand for devices and products required for respective procedures. For instance, Barco’s co-CEOs have recognized problems with the supply chain, producing value from technology, organizational structure, and R&D.

Longer intervals of peak loads in hospitals often produce an exponentially rising surgery waitlist of semi-urgent and non-urgent surgeries. The COVID-19 caused considerable wait times for patients standing by for surgery. A study published in the British Journal of Surgery showed that COVID-19 led to 28 million postponed or canceled surgeries globally in 2020 with millions of surgeries pushed into 2021. Thus, with thousands of patients facing delays in surgeries the necessity to enhance scheduling efficiencies has become more important. As a result, market players have introduced various technologies to cater to demand in the market for operating room integration. For instance, in June 2021, Getinge revealed that it released the “Torin” AI-based OR management system in the U.S.

Furthermore, the pandemic has pushed market players to operate in new ways, thus accelerating digitization. Operating rooms and surgical procedures changed in the following three ways in response to the pandemic-increased pre-surgical planning, video conferencing, and remote post-surgical patient engagement. Preoperative planning is already common in most areas of surgery. Shortly, there might be a better chance to take advantage of the preoperative phase of surgery, since preparations can be done with other clinicians in the office with negligible contact.

Gather more insights about the market drivers, restrains and growth of the Global Operating Room Integration Market

Detailed Segmentation:

Component Insights

The software segment dominated the market in 2022, owing to various benefits associated with its use. These integrated software solutions offer seamless communication within various systems operational in OR to streamline surgical workflows and ensure ease of use and effective operation. In addition, companies are also marking their presence in the market for operating room integration by adopting attainment strategies to broaden their portfolio in the operating room integration space.

Device Type Insights

The documentation management systems segment accounted for the largest revenue share of over 35.0% in the market for operating room integration in 2022 owing to its wide applications in ORs. This system helps in managing all the records from various sources and presents them on a single platform to help surgeons with patients’ history and other necessary information during the surgery. Operating rooms are increasingly becoming complex and congested with the inclusion of a variety of equipment such as surgical lights, operating tables, and surgical displays. In basic ORs, individual devices are arranged which are pulled or pushed back according to their use, cords and cables are spread all over the room. This heightens the risk of tripping or pulling out the essential cord during surgery or damaging any equipment. Integrated operating rooms (I-ORs) help to curb this problem.

Application Type Insights

The general surgery segment dominated the market for operating room integration and accounted for the largest revenue share of more than 30.0% in 2022. The increasing number of hospitals adopting MIS technology coupled with the rising number of chronic illnesses and requiring surgical procedures is further fueling the market growth. For instance, in the U.S. approximately half of the surgeries are done with MIS technology. The rising number of surgical interventions with the high number of MIS being carried out due to its several benefits such as reduced hospital stay, less painful features, and high focus on patient safety in OR are driving the demand. As this technology continues to grow along with telemedicine and robotic surgery becoming more common healthcare services, the I-ORs are expected to become an industry-standard in the coming years.

End-use Insights

The hospital segment dominated the market in 2021. This growth is owing to the high penetration of integrated ORs. With the large patient population being exposed to chronic diseases there is a need for I-ORs to reduce the burden on physicians and complexity so that they can efficiently manage their surgical workflow. Furthermore, ongoing technology innovations in medical devices attributing to the growing adoption of I-ORs over the forecast period.

Browse through Grand View Research's Healthcare Industry Research Reports.

Emergency Medical Services Product Market: The global emergency medical services product market size was valued at USD 22.5 billion in 2023 and is projected to grow at a CAGR of 6.4% from 2024 to 2030.

Nonmydriatic Fundus Cameras Market: The global nonmydriatic fundus cameras market size was valued at USD 173.5 million in 2023 and is projected to grow at a CAGR of 5.9% from 2024 to 2030.

Regional Insights

North America dominated the market and accounted for the largest revenue share of over 45.0% in 2022. Dominance can be attributed to the increasing demand for surgical automation. Major factors attributed to the market growth are the rise in demand for efficient healthcare services, an increase in the need to reduce healthcare expenditure, and effective EHR implementation by healthcare organizations. Furthermore, the presence of established players in the market, technologically advanced HCIT, and funding to improve OR infrastructure is other factors propelling the market growth.

Key Companies & Market Share Insights

The industry is fragmented with a large number of players operating in this sector. The key players are focusing on implementing new strategies such as regional expansion, mergers, and acquisitions, improving their application portfolio through innovation, partnerships, and distribution agreements to increase their revenue share and mark their presence in the market. For instance, in April 2021, Barco launched surgical teleconferencing, telementoring, and teleassistance solution called NexxisLive as a secure cloud-based platform for ORs. While, in April 2021, caresyntax’s digital surgery platform was selected as part of a pilot program by the American Board of Surgery to enhance surgeon certifications with video-based assessments.

Likewise in January 2020, Caresyntax announced the installation of 16 digital ORs in Calvary Adelaide Hospital in South Australia with its digital OR integration platform, PRIME365. These types of initiatives are attributing to the increasing penetration of I-ORs in the coming years. Furthermore, Innovations like these by the established market players focused on introducing integrated OR platform globally is likely to propel market growth. Some of the prominent players in the operating room integration market include:

Braiblab AGBarcoDragerwerk AG & Co. KGaASteris Plc.KARL STORZ SE & CO. KGOlympusCare SyntaxArthrex, Inc.Stryker CorporationOlympus CorporationGetinge ABALVO MedicalSkytron, LLC,MerivaaraTRILUX Medical GmbH & Co. KGCaresyntaxSony CorporationRichard Wolf GmbHFUJIFILM Holdings CorporationDitec MedicalDoricon Medical SystemsHill-Rom Holdings, Inc.EIZO GmbHOPExPARKISIS-Surgimedia,MeditekZimmer Biomet Holdings, Inc.

Order a free sample PDF of the Operating Room Integration Market Intelligence Study, published by Grand View Research.