Chemical Mechanical Planarization (CMP) Slurry Market

Introduction

The Chemical Mechanical Planarization (CMP) Slurry market plays a pivotal role in the semiconductor manufacturing ecosystem, serving as a critical consumable in the planarization process of semiconductor wafers. CMP slurry is a specialized chemical formulation used to polish and smooth wafer surfaces during the production of integrated circuits, enabling precise patterning and multilayered chip architecture. As the demand for smaller, faster, and more efficient electronic devices continues to grow, the need for advanced CMP solutions becomes increasingly vital.

Driven by the rapid advancement in semiconductor technologies, the CMP slurry market is witnessing significant growth, particularly in applications involving logic chips, memory devices, and advanced packaging. The industry is also being shaped by evolving materials such as low-k dielectrics, copper interconnects, and 3D NAND, which require tailored slurry compositions to meet specific planarization and defect control requirements.

Chemical Mechanical Planarization (CMP) Slurry Market Size

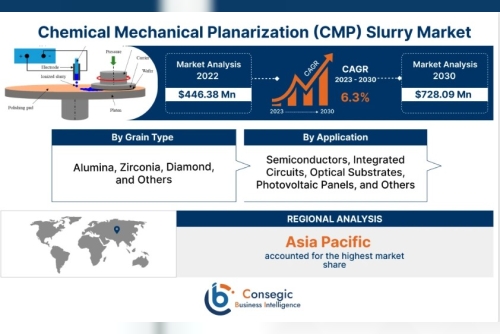

Consegic Business Intelligence analyzes that the Chemical Mechanical Planarization (CMP) Slurry Market size is estimated to reach over USD 854.3 Million by 2032 from a value of USD 525.62 Million in 2024 and is projected to grow by USD 549.15 Million in 2025, growing at a CAGR of 6.3 % from 2025 to 2032.

Chemical Mechanical Planarization (CMP) Slurry Market Scope & Overview

The Chemical Mechanical Planarization (CMP) Slurry market encompasses a specialized segment within the semiconductor materials industry, focusing on the development, production, and application of slurry formulations used in the CMP process. This process is essential for achieving the high level of surface flatness required in modern semiconductor manufacturing, particularly in advanced nodes and multi-layered device structures.

The market includes various slurry types—such as oxide, metal (copper, tungsten), and dielectric slurries—each tailored for specific materials and device layers. These formulations typically contain abrasive particles, chemical agents, stabilizers, and surfactants, all engineered to deliver optimal removal rates, selectivity, and defect control.

Scope of the Report:

By Material Type: Oxide Slurry, Copper Slurry, Tungsten Slurry, Cobalt Slurry, Others By Application: Memory Devices, Logic Devices, Foundry, Advanced Packaging, Others By End-User: Integrated Device Manufacturers (IDMs), Foundries, Outsourced Semiconductor Assembly and Test (OSAT) companies By Region: North America, Europe, Asia-Pacific, Latin America, Middle East & AfricaThe report offers a detailed examination of market dynamics including drivers such as rising demand for high-performance chips, technological advancements in wafer fabrication, and the miniaturization of semiconductor devices. It also analyzes constraints such as the high cost of R&D, environmental concerns, and the complexity of developing application-specific slurry chemistries.

Furthermore, the overview highlights key market participants, recent product innovations, strategic collaborations, and emerging opportunities in advanced packaging, 3D integration, and AI-driven semiconductor design. The study period of 2025 to 2032 provides insights into short-, mid-, and long-term growth prospects.

Chemical Mechanical Planarization (CMP) Slurry Market Dynamics (DRO)

Drivers:

Rising Demand for Advanced Semiconductor DevicesThe global push for smaller, faster, and more power-efficient electronic devices is accelerating the adoption of advanced semiconductor nodes (7nm, 5nm, and beyond), driving demand for high-performance CMP slurry solutions. Growth in 3D NAND and Logic Chip Production

Increasing deployment of 3D NAND memory and high-performance logic chips in AI, data centers, and mobile devices necessitates precise planarization, boosting slurry consumption. Expansion of Semiconductor Manufacturing Facilities

Significant investments in new semiconductor fabs, particularly in Asia-Pacific, the U.S., and Europe, are creating steady demand for CMP consumables, including slurries. Technological Innovations in CMP Slurry Formulations

Continuous improvements in slurry selectivity, removal rate, defectivity reduction, and compatibility with novel materials (like cobalt and low-k dielectrics) are enhancing product performance and market growth.

Restraints:

High Cost of R&D and CustomizationDeveloping application-specific slurry chemistries is complex and expensive, posing challenges for smaller market players and slowing time-to-market for new solutions. Environmental and Waste Management Concerns

Disposal and treatment of used slurry materials pose environmental challenges and regulatory pressures, especially in regions with strict environmental policies. Supply Chain Volatility and Raw Material Dependency

Fluctuations in the availability and cost of raw materials, such as abrasive particles and specialty chemicals, can affect production costs and profit margins.

Opportunities:

Emergence of Advanced Packaging TechnologiesGrowing adoption of chiplet architectures, system-in-package (SiP), and fan-out packaging is creating new slurry demand for heterogeneous integration processes. Sustainability and Green Chemistry Initiatives

Rising interest in eco-friendly and recyclable slurry formulations opens the door for innovation and differentiation, especially among environmentally conscious manufacturers. Expansion in Emerging Markets

Countries like India, Vietnam, and Malaysia are investing in semiconductor infrastructure, offering untapped growth opportunities for CMP slurry providers.

Chemical Mechanical Planarization (CMP) Slurry Market Segmental Analysis

By Grain Type:

Silica-Based Slurry Most commonly used grain type in oxide and shallow trench isolation (STI) processes. Offers excellent uniformity and cost-efficiency. Dominates in planarization of dielectric materials. Alumina-Based Slurry Primarily used for metal CMP, especially copper and tungsten. Provides high material removal rates and is suitable for harder surfaces. Ceria-Based Slurry Known for superior selectivity and low defectivity, often used in advanced nodes and ILD (Interlayer Dielectric) CMP. Gaining popularity in applications demanding high precision. Others (Zirconia, Manganese Oxide, Hybrid Grains) Used for niche and emerging applications requiring specific chemical/mechanical characteristics. Hybrid and engineered grains are being explored for next-gen CMP needs.By Application:

Memory Devices Includes DRAM and 3D NAND. CMP is critical for planarizing multiple layers and ensuring structural integrity. Logic Devices Used in CPUs, GPUs, and SoCs. Requires precise and defect-free planarization, especially at nodes below 7nm. Foundry & IDM High-volume fabs utilize customized slurries for process integration and yield optimization. Increasing demand from global foundry leaders. Advanced Packaging (e.g., TSV, WLCSP, Fan-out) Rising due to the popularity of chiplet and heterogeneous integration designs. Requires specialized slurry for through-silicon vias and redistribution layers. Others (LEDs, MEMS, Optical Devices) Emerging applications expanding the scope of CMP slurry demand beyond traditional semiconductor uses.By Region:

Asia-Pacific Leading Region, driven by major semiconductor hubs in China, South Korea, Taiwan, and Japan. Strong presence of foundries and IDMs fuels continuous CMP slurry consumption. North America Significant demand from leading chipmakers and R&D centers in the U.S. Government support for semiconductor independence boosts local production. Europe Moderate growth supported by advanced research, specialty semiconductors, and automotive electronics demand. EU investments in semiconductor sovereignty support market development. Latin America Emerging market with potential for growth through foreign investment and regional semiconductor initiatives. Middle East & Africa Nascent market; long-term potential tied to tech diversification strategies in countries like UAE and Israel.

Top Key Players & Market Share Insights

The global Chemical Mechanical Planarization (CMP) Slurry market is highly competitive, with several key players leading in innovation, product development, and strategic collaborations. These companies play a crucial role in shaping the market landscape by supplying advanced slurry solutions tailored to diverse semiconductor applications.

Leading Market Players:

Hitachi, Ltd. Fujifilm Corporation Cabot Microelectronics Corporation Fujimi Corporation Merck KGaA DuPont Saint-Gobain Ceramics & Plastics, Inc. BASF SE Showa Denko Materials Co. Ltd AGC Inc.

Contact Us:

Consegic Business intelligence

Email : [email protected]

Sales : [email protected]