Cut and Stack Labels Market

Introduction

The Cut and Stack Labels Market plays a vital role in the global packaging and labeling industry, offering versatile and cost-effective solutions for a wide range of products. These labels are typically printed on large sheets, cut into individual pieces, and then stacked for application, making them highly suitable for high-volume labeling requirements. They are widely used in industries such as food and beverages, personal care, household products, pharmaceuticals, and chemicals due to their durability, high print quality, and ability to accommodate detailed graphics and branding. The market is being driven by growing consumer demand for attractive packaging, brand differentiation strategies, and advancements in printing technologies. Additionally, the increasing adoption of sustainable and recyclable label materials is reshaping the industry, as companies aim to meet eco-friendly packaging standards while maintaining cost efficiency and design flexibility.

Cut and Stack Labels Market Size

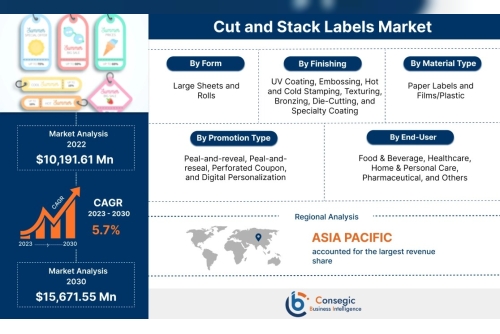

Cut and Stack Labels Market is estimated to reach over USD 15,671.55 Million by 2030 from a value of USD 10,191.61 Million in 2022, growing at a CAGR of 5.7% from 2023 to 2030.

Cut and Stack Labels Market: Definition & Overview

Definition:

Cut and stack labels are a type of product labeling solution produced by

printing large sheets of paper or film, which are then cut into individual

labels and stacked for easy application. Unlike pressure-sensitive or shrink

sleeve labels, these labels require glue or adhesive during application, making

them especially cost-effective for high-volume production runs.

Overview:

The Cut

and Stack Labels Market represents a significant segment of the global

labeling industry, valued for its affordability, versatility, and wide

applicability across multiple sectors. These labels are predominantly used in

industries such as food and beverages, personal care, household goods,

chemicals, and pharmaceuticals. They allow for high-quality printing, detailed

graphics, and vibrant designs, which help enhance brand visibility and consumer

appeal. With the increasing focus on sustainable packaging, manufacturers are

also adopting eco-friendly substrates, recyclable inks, and water-based

adhesives for cut and stack labels. Market growth is further supported by

rising demand for customized branding, cost-efficient labeling solutions, and

innovations in printing technologies such as offset, flexographic, and digital

printing. This positions cut and stack labels as a reliable and competitive

choice in modern packaging strategies.

Cut and Stack Labels Market Dynamics (DRO)

1. Drivers

Rising demand for cost-effective labeling solutions: Cut and stack labels are highly economical for large-scale production, making them attractive for mass-market products. Increasing consumption of packaged food and beverages: Growing urbanization and lifestyle changes are fueling demand for packaged goods, boosting label requirements. Advancements in printing technologies: Innovations in offset, flexographic, and digital printing enhance design flexibility, print quality, and production efficiency. Focus on branding and product differentiation: Companies use vibrant and customizable labels to strengthen shelf appeal and consumer engagement. Adoption of eco-friendly materials: Rising environmental awareness is driving the use of recyclable papers, films, and water-based inks in label production. Expanding industrial applications: Beyond food and beverages, labels are being widely used in pharmaceuticals, chemicals, and personal care packaging.2. Restraints

Dependency on adhesives: Application requires glue, which can increase process complexity and limit speed compared to self-adhesive labels. Competition from alternative labels: Shrink sleeves, pressure-sensitive, and in-mold labels offer better durability and convenience, limiting cut and stack adoption. Moisture and durability limitations: These labels can face issues in humid or harsh environments without protective coatings. Environmental concerns: Use of non-recyclable materials and inks can pose sustainability challenges for manufacturers. High setup cost for small runs: Printing large sheets and cutting them is not cost-efficient for limited production, restricting use by smaller brands.3. Opportunities

Sustainable material innovation: Development of biodegradable and recyclable label substrates offers growth prospects in eco-conscious markets. Emerging market expansion: Rapid urbanization and growing disposable incomes in Asia-Pacific, Latin America, and Africa are driving demand for affordable packaging. Integration of smart features: Adding QR codes, NFC tags, and track-and-trace elements enhances product security and consumer interaction. Growth of e-commerce and retail sectors: Attractive labels improve unboxing experience and help brands stand out in competitive online and offline shelves. Collaborations and partnerships: Printers and packaging firms are teaming up to deliver innovative and cost-optimized labeling solutions. Trend toward customizable packaging: Increasing preference for lightweight, flexible, and personalized packaging formats is boosting cut and stack label demand.

Cut and Stack Labels Market — Segmental Analysis

By Form

Sheet Labels (Single-Face): Labels printed on single sheets then cut and stacked; widely used for simple, cost-effective applications. Multi-Panel / Wraparound Labels: Larger sheets cut to wrap around containers (e.g., bottles); useful for extended artwork and product information. Die-Cut Labels: Sheets containing individually die-cut shapes ready for stacking, enabling complex shapes and premium finishes.By Finishing

Gloss Finish: Provides high-sheen appearance and vibrant colors, commonly used for premium consumer goods to boost shelf appeal. Matte Finish: Non-reflective, elegant look that hides imperfections and is preferred for upscale or natural/organic product positioning. UV Coating / Varnish: Adds surface protection and enhances visual contrast; available as spot or full-coverage for durability and accentuation. Lamination (Film Laminate): Adds moisture and abrasion resistance for labels exposed to harsh conditions or refrigerated supply chains.By Material Type

Paper Substrates: Cost-effective and widely recyclable; commonly used for dry-goods and general consumer packaging. Film (Polypropylene / PET): Offers superior moisture resistance and durability, suitable for wet or refrigerated products. Specialty / Synthetic Papers: Blend of paper and polymers that balance printability with improved tear and moisture resistance. Eco / Biodegradable Substrates: Compostable or bio-based materials aimed at sustainability-focused brands and regulations.By Promotion Type

Standard/Brand Labels: Regular branding and product information labels used in mainstream product packaging. Promotional/Seasonal Labels: Limited-edition or promotional runs for campaigns, festivals, or sales events to stimulate purchase. Security / Tamper-Evident Labels: Incorporate void patterns or destructible materials to prevent tampering and ensure product integrity. Interactive / Smart Labels: Include QR codes, NFC chips or variable data for consumer engagement, traceability, and anti-counterfeiting.By End-User

Food & Beverage: Largest end-user segment; requires attractive, regulatory-compliant labeling and often moisture-resistant finishes. Pharmaceuticals & Healthcare: Demands high accuracy, batch/expiry data, and tamper-evident or serialized labeling for compliance. Personal Care & Cosmetics: Emphasizes premium graphic quality, unique shapes, and luxury finishes to support brand image. Household & Industrial Chemicals: Needs durable, chemical-resistant labels with safety and instruction information. Automotive & Electronics: Uses durable film labels for component identification, safety markings, and long lifecycle performance. Retail & Logistics: Includes barcode and SKU labels for inventory, promotional tagging, and supply-chain visibility.By Region

North America: Mature market driven by branding, regulatory compliance, and demand for specialty/smart labels. Europe: Strong sustainability focus and stringent labeling regulations encourage recyclable materials and high-quality finishes. Asia-Pacific: Fastest growing region due to rising FMCG production, expanding retail/e-commerce, and cost-sensitive demand. Latin America: Growing packaged goods market with increasing adoption of modern printing and finishing technologies. Middle East & Africa: Emerging demand tied to urbanization and imports, with opportunities in food & beverage and consumer goods sectors.

Top Key Players & Market Share Insights

Anacotte Packaging Resource Label Group Blue Label Packaging Inland Packaging CPC Packaging Atlas Labels & Packaging The New Label Printing Company Smyth Companies Pixelle Specialty Solutions Gallus Avery Products Corporation