Digital TV Market

Introduction

The Digital TV Market is experiencing significant growth as advancements in broadcasting technology, rising internet penetration, and increasing consumer demand for high-quality content transform the entertainment landscape. Digital television offers enhanced picture and sound quality compared to traditional analog systems, along with interactive features, on-demand services, and seamless integration with smart devices. The market is being driven by the rapid adoption of smart TVs, expansion of over-the-top (OTT) platforms, and the shift from cable and satellite broadcasting to internet-based streaming services. Additionally, government initiatives to promote digital broadcasting and the continuous rollout of high-definition (HD) and ultra-high-definition (UHD/4K) content are further boosting adoption. With growing consumer preference for personalized viewing experiences and connected entertainment ecosystems, the Digital TV Market is set to expand robustly between 2025 and 2032.

Digital TV Market Size

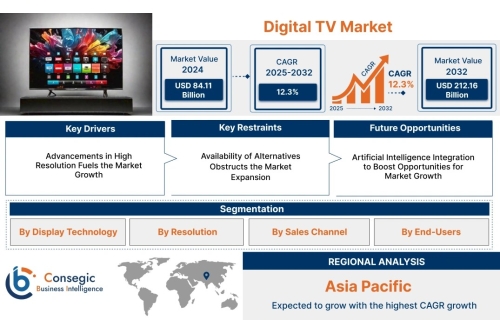

Digital TV Market size is estimated to reach over USD 212.16 Billion by 2032 from a value of USD 84.11 Billion in 2024 and is projected to grow by USD 92.93 Billion in 2025, growing at a CAGR of 12.3% from 2025 to 2032.

Digital TV Market Scope & Overview

The Digital TV Market scope encompasses a wide range of technologies, products, and services that enable digital broadcasting and content delivery across multiple platforms. It includes terrestrial, cable, satellite, and internet protocol television (IPTV), as well as smart TVs and integrated streaming solutions. The market overview highlights the transition from analog to digital broadcasting, driven by the demand for superior audio-visual quality, interactive features, and seamless connectivity. Key factors influencing the market include the growing popularity of OTT platforms, rising household penetration of smart TVs, and advancements in 4K and 8K resolution displays. The market also covers various end-users, including residential, commercial, and hospitality sectors. With regulatory support for digital migration, continuous technological innovation, and expanding digital infrastructure, the Digital TV Market is poised for steady growth during 2025–2032.

Digital TV Market Dynamics (DRO)

1. Drivers

Rising Demand for High-Quality Content: Growing consumer preference for HD, 4K, and 8K video quality is fueling the adoption of digital TVs. Expansion of OTT Platforms: Streaming services such as Netflix, Amazon Prime, and Disney+ are boosting the demand for smart and internet-enabled TVs. Government Initiatives for Digital Broadcasting: Many countries are phasing out analog broadcasting and mandating digital migration, driving market growth. Technological Advancements: Integration of AI, voice assistance, and IoT features in smart TVs is enhancing user experience and market penetration.2. Restraints

High Initial Costs: Advanced digital TVs and smart TVs come with higher purchase and installation costs, limiting affordability in price-sensitive regions. Infrastructure Limitations: In developing countries, lack of reliable internet connectivity and broadcasting infrastructure hampers market growth. Content Piracy Concerns: Illegal streaming and piracy of digital content pose challenges to revenue generation for service providers.3. Opportunities

Emerging Markets Adoption: Rising disposable income and digital infrastructure expansion in Asia-Pacific, Africa, and Latin America present strong growth opportunities. Integration with Smart Ecosystems: The growing trend of smart homes and connected devices is opening new avenues for digital TV integration. Advertising & Monetization Models: Innovative advertising formats and targeted ads on digital platforms are creating revenue streams for stakeholders.

Digital TV Market Segmental Analysis

1. By Display Technology

LCD (Liquid Crystal Display): Widely used due to affordability and energy efficiency, dominating the mid-range TV segment. LED (Light Emitting Diode): Offers enhanced brightness and better contrast, making it the most popular display choice globally. OLED (Organic Light Emitting Diode): Known for superior picture quality, deep blacks, and slim design, catering to premium customers. QLED (Quantum Dot LED): Provides vibrant colors and high brightness, gaining traction in high-end and large-screen TVs.2. By Resolution

HD (High Definition): Still relevant in developing countries due to lower cost and adequate picture quality. Full HD (FHD): A balanced option with good clarity, widely adopted in mid-range TVs. 4K Ultra HD: Becoming mainstream, driven by streaming platforms offering UHD content. 8K Ultra HD: Emerging technology targeting premium users, expected to grow with wider content availability.3. By Sales Channel

Online Sales: E-commerce and brand-owned online platforms are boosting sales with discounts, wide variety, and convenience. Offline Sales: Retail stores, electronics showrooms, and hypermarkets remain important for customers preferring hands-on experience.4. By End User

Residential: Accounts for the largest share as households increasingly shift to smart and connected TVs. Commercial: Includes hotels, restaurants, and retail outlets using digital TVs for entertainment and promotions. Educational Institutions: Growing use of digital TVs for e-learning and interactive classrooms. Corporate Offices: Adoption in meeting rooms and lobbies for presentations and information displays.5. Regional Analysis

North America: Mature market with strong penetration of smart TVs and high OTT platform usage. Europe: Driven by digital switchover policies and strong demand for advanced display technologies. Asia-Pacific: Fastest-growing region, led by China, India, and Japan due to rising income levels and internet adoption. Latin America: Expanding market with increasing OTT consumption and digital migration initiatives. Middle East & Africa: Growth supported by improving digital infrastructure and rising consumer spending.

Top Key Players & Market Share Insights

Samsung Electronics (South Korea) LG Electronics (Japan) Panasonic Corporation (Japan) Apple Inc (US) Toshiba Corporation (Japan) Sony Corporation (Japan) Hisense (China) Haier (China) PHILIPS (Netherlands) Xiaomi (China)

Contact Us:

Consegic Business intelligence

Email : [email protected]

Sales : [email protected]