Electric Vehicle Fast Charging System Market

Introduction

The Electric Vehicle (EV) Fast Charging System market is experiencing rapid growth, driven by the increasing adoption of electric vehicles worldwide and the urgent need for efficient and convenient charging solutions. As governments and industries intensify efforts to reduce carbon emissions and transition toward sustainable mobility, fast charging infrastructure has become a critical component in supporting the widespread use of EVs. Fast charging systems significantly reduce charging time compared to conventional chargers, making them essential for long-distance travel, urban transportation, and commercial fleet operations.

This market encompasses a variety of technologies, including DC fast chargers, ultra-fast chargers, and wireless charging systems, with major advancements focused on enhancing charging speed, interoperability, and grid integration. Key players in the automotive and energy sectors are investing heavily in research and development, infrastructure deployment, and strategic partnerships to expand their market presence. As a result, the EV fast charging system market is poised for robust expansion, driven by technological innovations, regulatory incentives, and growing consumer demand for cleaner, more efficient transportation solutions.

Electric Vehicle Fast Charging System Market Scope & Overview

The Electric Vehicle (EV) Fast Charging System market encompasses a broad range of technologies, infrastructure solutions, and services designed to enable rapid charging of electric vehicles. This market includes hardware components such as DC fast chargers, ultra-fast chargers (150 kW and above), and supporting electrical infrastructure, as well as software solutions for payment systems, remote monitoring, and energy management. The scope of the market extends across various vehicle types, including passenger cars, commercial vehicles, and public transport systems.

The market also covers different charging levels and standards (such as CHAdeMO, CCS, and GB/T), as well as deployment settings like highways, urban charging stations, commercial parking facilities, and residential areas. Key stakeholders include automotive manufacturers, utility providers, charging infrastructure developers, and government agencies.

Electric Vehicle Fast Charging System Market Size

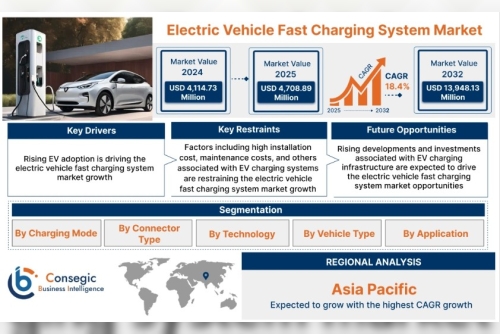

Electric Vehicle Fast Charging System Market size is estimated to reach over USD 13,948.13 Million by 2032 from a value of USD 4,114.73 Million in 2024 and is projected to grow by USD 4,708.89 Million in 2025, growing at a CAGR of 18.4% from 2025 to 2032.

Electric Vehicle Fast Charging System Market Dynamics (DRO)

1. Drivers:

Rising Adoption of Electric Vehicles (EVs): Increasing global shift towards sustainable transportation is driving demand for fast charging infrastructure. Government Initiatives and Incentives: Supportive policies, subsidies, and funding for EV infrastructure development are accelerating market growth. Advancements in Charging Technology: Innovations in fast charging (e.g., ultra-fast and high-power chargers) are improving charging speeds and efficiency. Urbanization and Smart City Projects: Growing urban mobility needs and smart city developments are creating a strong demand for public fast charging stations. Partnerships and Collaborations: Strategic alliances between automotive companies, utility firms, and tech providers are enhancing infrastructure rollout.2. Restraints:

High Initial Investment and Installation Costs: Deployment of fast charging systems requires substantial capital, which can deter small operators. Grid Capacity and Power Supply Challenges: Fast chargers demand high energy loads, putting pressure on existing grid infrastructure. Limited Standardization: Variations in charging standards and connector types across regions can hinder universal access and interoperability. Maintenance and Operational Complexity: The need for regular maintenance and complex backend operations can increase total cost of ownership.3. Opportunities:

Expansion into Emerging Markets: Developing countries with growing EV adoption present untapped potential for infrastructure development. Integration with Renewable Energy: Combining fast chargers with solar, wind, or energy storage systems offers a path toward sustainable charging solutions. Wireless and Smart Charging Innovations: Emerging technologies such as wireless charging and AI-driven energy management systems provide new growth avenues. Fleet Electrification: Rising demand for electrified commercial fleets and public transport boosts the need for reliable, high-capacity fast charging networks.

Electric Vehicle Fast Charging System Market Segmental Analysis

1. By Charging Mode:

Plug-in Charging: The most widely used mode, requiring physical connection between the EV and the charger via a cable. Wireless Charging: An emerging technology that allows energy transfer through electromagnetic fields, offering convenience and automation.2. By Connector Type:

Combined Charging System (CCS): A widely adopted standard in Europe and North America, offering both AC and DC charging through a single port. CHAdeMO: A fast-charging standard originating from Japan, known for its bidirectional charging capabilities. GB/T: The Chinese standard for electric vehicle charging, used widely in China. Tesla Supercharger: A proprietary charging connector used by Tesla vehicles, primarily in their own network.3. By Technology:

DC Fast Charging: Offers high power output (typically 50 kW and above), ideal for quick top-ups on long journeys. Ultra-Fast Charging: Provides significantly higher output (up to 350 kW), enabling charging within minutes. Smart Charging Systems: Integrate with energy management systems and IoT platforms for efficient and optimized charging.4. By Vehicle Type:

Passenger Cars: Major market segment due to the rapid increase in EV adoption among consumers. Commercial Vehicles: Includes delivery vans, buses, and trucks, which require higher power and faster turnaround. Two-Wheelers and Three-Wheelers: Gaining traction in Asia-Pacific and developing regions with rising urban mobility needs.5. By Application:

Residential Charging: Home-based chargers, often slower but convenient for overnight charging. Commercial Charging: Installed at workplaces, shopping centers, and public parking areas for customer and employee use. Public Charging: High-power stations located on highways, urban centers, and transport hubs, critical for intercity travel. Fleet Charging: Dedicated infrastructure for commercial fleet operators, logistics firms, and public transport authorities.6. Regional Analysis:

North America: Rapid expansion of charging infrastructure, government incentives, and strong presence of EV manufacturers. Europe: Leading in EV adoption, supported by stringent emission regulations and large-scale infrastructure projects. Asia-Pacific: Fastest-growing region with major contributions from China, Japan, and South Korea, driven by government policies and urbanization. Latin America: Emerging market with growing awareness and pilot infrastructure projects in key countries like Brazil and Mexico. Middle East & Africa: Nascent stage but showing interest through sustainable development initiatives and diversification efforts.

Top Key Players and Market Share Insights

ChargePoint (US) Blink Charging (US) ABB Ltd (Switzerland) EVgo (US) Wallbox (Spain) Charge Zone (India) Tata Power (India) Ather Energy (India) Siemens AG (Germany) Tesla (US)

Contact Us:

Consegic Business intelligence

Email : [email protected]

Sales : [email protected]