Food Automation Market

Introduction

The Food

Automation Market is witnessing strong growth as food manufacturers

increasingly adopt automation technologies to enhance efficiency, safety, and

productivity. Automation solutions such as robotics, processing equipment,

control systems, and packaging technologies are transforming the food industry

by streamlining operations, reducing labor costs, and ensuring consistent

product quality. Rising consumer demand for packaged and processed foods,

coupled with strict food safety regulations, is driving the adoption of automated

solutions across production lines. Additionally, the growing need for real-time

monitoring, energy efficiency, and smart manufacturing practices is further

accelerating market expansion, making food automation a critical component of

the modern food processing ecosystem.

Food Automation Market Size

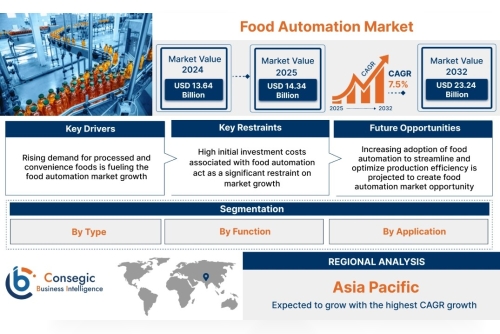

Food Automation Market Size is estimated to reach over USD 23.24 Billion by 2032 from a value of USD 13.64 Billion in 2024 and is projected to grow by USD 14.34 Billion in 2025, growing at a CAGR of 7.5% from 2025 to 2032.

Food

Automation Market Scope & Overview

The Food

Automation Market encompasses advanced technologies, systems, and

equipment designed to optimize various stages of food production, processing,

and packaging. Its scope includes robotics, control systems, conveyors,

processing machinery, and vision inspection systems that enhance efficiency,

safety, and scalability. The market is expanding rapidly due to increasing

demand for processed and packaged foods, stringent food safety standards, and

the industry’s shift toward smart factories and Industry 4.0 practices. Automation

also addresses challenges such as labor shortages, production consistency, and

energy management, making it an essential solution for both large-scale

manufacturers and small food processing units. With continuous advancements in

robotics, AI, IoT, and machine learning, the food automation market is poised

for significant growth, offering improved productivity, reduced operational

costs, and enhanced quality assurance across global food supply chains.

Food Automation Market Dynamics (DRO)

Drivers:

Rising demand for processed and packaged food products driving automation adoption. Strict food safety and hygiene regulations encouraging the use of automated systems. Labor shortages and high labor costs pushing food manufacturers toward automation. Growing implementation of Industry 4.0, IoT, and AI technologies in food processing.Restraints:

High initial investment costs for automation equipment and integration. Limited adoption among small and medium-sized food processing units due to budget constraints. Technical complexities and need for skilled workforce to manage advanced systems. Concerns over system downtime and maintenance affecting productivity.Opportunities:

Increasing use of robotics and AI-driven solutions for precision and efficiency. Rising demand for energy-efficient and sustainable automation technologies. Growth in emerging markets with expanding food processing industries. Development of smart packaging and real-time monitoring systems enhancing product traceability.

Food Automation Market Segmental Analysis:

By Type:

Motors & Generators: Essential for driving automated equipment across food processing units. Robotics: Increasingly used in packaging, sorting, and handling tasks for precision and efficiency. Control Systems: PLCs, SCADA, and DCS systems for process monitoring and automation control. Conveyors & Sortation Systems: Streamlining material handling and reducing manual intervention. Sensors & Machine Vision Systems: Ensuring quality control, defect detection, and safety compliance. Others: Includes actuators, drives, and auxiliary automation components.By Function:

Processing: Automation in mixing, blending, cutting, and cooking operations. Packaging & Repackaging: Robotics and automated machinery for filling, sealing, labeling, and wrapping. Palletizing & Depalletizing: Automated stacking, sorting, and material handling solutions. Sorting & Grading: Vision and sensor-based automation for quality assurance. Others: Includes cleaning, sanitation, and inspection systems.By Application:

Bakery & Confectionery: Automation for dough mixing, baking, decorating, and packaging. Beverages: Used in bottling, labeling, filling, and quality testing. Dairy & Frozen Foods: Automation in pasteurization, packaging, and cold-chain management. Meat, Poultry & Seafood: Robotic cutting, portioning, deboning, and packaging solutions. Fruits & Vegetables: Sorting, grading, washing, and packaging automation. Others: Functional foods, ready-to-eat meals, and convenience foods.Regional Analysis:

North America: Leading market driven by advanced food processing infrastructure and strict safety regulations. Europe: Growth supported by strong adoption of robotics and sustainable food automation technologies. Asia-Pacific: Fastest-growing market fueled by rising processed food demand and industrialization. Latin America: Expanding adoption in beverage and meat processing industries. Middle East & Africa: Moderate growth with increasing investments in modern food processing facilities.

Top Key Players and Market Share Insights

ABB (Switzerland) Siemens AG (Germany) Rockwell Automation Inc. (USA) Mitsubishi Electric Corporation (Japan) Schneider Electric SE (France) GEA Group (Germany) Emerson Electric Co. (USA) Yokogawa Electric Corporation (Japan) FANUC (Japan) KUKA AG (Germany) Honeywell International Inc. (USA) Omron Automation (Japan) Yaskawa Electric Corporation (Japan) Rexnord Corporation (Regal Rexnord Corporation) (USA) Fortive Corporation (USA)

Contact Us:

Consegic Business intelligence

Email : [email protected]

Sales : [email protected]

اجاره دستگاه اکسیژن ساز – The Smart Rental Hack You Must Know!

اجاره دستگاه اکسیژن ساز – The Smart Rental Hack You Must Know!