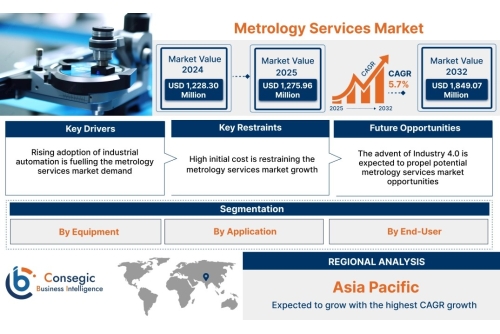

Metrology Services Market

Introduction

The Metrology Services Market is experiencing steady growth driven by rising demand for accuracy and precision across various industrial verticals. These services help manufacturers reduce product defects, optimize production efficiency, and comply with international quality standards. Industries such as aerospace, automotive, semiconductor manufacturing, and medical devices depend heavily on accurate measurements to maintain reliability and safety. Advanced metrology tools including 3D scanning, optical imaging, CMM systems, and laser measurement systems are increasingly replacing traditional measurement methods. The trend toward automation, robotics, additive manufacturing, and Industry 4.0 is further expanding the role of metrology in smart factories. Outsourcing metrology has become common due to cost savings and access to advanced equipment. Emerging technologies such as cloud-based metrology, AI-driven inspection systems, digital twins, and predictive quality analytics are transforming quality control processes. With increasing product complexity and global production networks, metrology services are becoming a core component of modern manufacturing strategies. Growing regulatory compliance requirements, certification standards, and defect prevention frameworks continue to strengthen demand for advanced measurement solutions across industries.

Metrology Services Market Size

Metrology Services Market size is estimated to reach over USD 1,849.07 Million by 2032 from a value of USD 1,228.30 Million in 2024 and is projected to grow by USD 1,275.96 Million in 2025, growing at a CAGR of 5.7% from 2025 to 2032.

Metrology Services Market Scope & Overview

The Metrology Services Market includes a wide range of offerings such as dimensional measurement, calibration, inspection, and digital analysis services. The market supports multiple industrial applications ranging from prototyping and reverse engineering to full-scale production and compliance testing. It includes on-site solutions, portable instruments, and laboratory-based metrology setups based on user requirements. The scope extends to both contact and non-contact metrology technologies including optical, laser, tactile, and automated measurement systems. As manufacturing evolves with advanced robotics and digital transformation, demand for intelligent and automated metrology solutions continues to increase. Subscription-based and value-added metrology services are gaining momentum due to flexibility and cost efficiency. Cloud integration and real-time analysis are making metrology an integral part of digital manufacturing frameworks. The market also includes training, technical support, system integration, and consulting for quality improvement programs.

Metrology Services Market Dynamics

Drivers

Growing Demand for High Precision ManufacturingIndustries such as aerospace, automotive, and semiconductor manufacturing require extremely tight tolerances. Increasing complexity in product design is further driving the need for advanced metrology solutions. Industry 4.0 and Digital Transformation

Smart factories are adopting connected metrology platforms to enable automated measurements, digital twins, and real-time quality monitoring. This shift improves efficiency and reduces manual inspection errors. Growth of Additive Manufacturing and 3D Printing

As 3D printing continues expanding into mainstream production, metrology becomes essential for verifying layer geometry, dimensional accuracy, and structural consistency of printed components. Rise in Outsourced Metrology Services

Many companies are shifting toward service-based metrology instead of purchasing expensive equipment. Outsourcing provides access to advanced tools while reducing capital investment and training requirements. Increasing Regulatory Emphasis on Quality and Compliance

Certifications like ISO, FDA, AS9100, and CE standards require strict measurement validation. Industries with critical safety and performance requirements rely heavily on metrology to meet certification benchmarks.

Restraints

High Cost of Advanced Metrology TechnologiesEquipment such as CMMs, laser trackers, and optical metrology systems require large capital investment. Maintenance, calibration, and training add additional ongoing costs. Shortage of Skilled Workforce

Operating advanced metrology tools requires specialized expertise. The shortage of trained professionals limits adoption, especially in developing markets. Complex Integration with Legacy Systems

Traditional factories with outdated production lines struggle to integrate modern digital inspection systems, slowing transformation. Variability in Measurement Standards Across Regions

Different country-level calibration and quality benchmarks create challenges for global manufacturers, leading to longer validation cycles.

Opportunities

Expansion in Emerging Industrial MarketsCountries in Asia-Pacific, Middle East, and Latin America are investing in manufacturing hubs, creating new demand for modern quality inspection services. Increasing Adoption of Portable and Mobile Metrology Systems

Portable 3D scanners and handheld measurement devices are creating new market opportunities by enabling flexible, on-site inspection. Growth in EVs, Renewable Energy, and Space Technologies

Emerging sectors require extremely high precision in components such as batteries, turbines, sensors, and propulsion systems—creating new metrology revenue streams. Artificial Intelligence and Machine Learning Advancements

AI-enabled inspection improves defect detection accuracy, reduces variability, and automates analysis, creating opportunities for scalable deployment.

Metrology Services Market Segmental Analysis

By Equipment

Coordinate Measuring Machines (CMMs)Widely used for precise dimensional measurement in aerospace and automotive sectors. Offers high accuracy with automated and programmable capabilities. Optical Digitizers and Scanners

Non-contact technology enabling high-speed scanning of complex geometries. Increasingly used in reverse engineering and additive manufacturing. Laser Trackers

Provide portable precision measurement for large-scale components. Commonly used in aircraft assembly, heavy machinery, and industrial calibration. Vision Measuring Systems

Used for high-resolution inspection of delicate and miniature components. Popular in semiconductor, medical device, and electronics manufacturing. Surface and Form Measurement Instruments

Used to inspect micro-level irregularities, textures, and tolerances. Critical for engineering applications that require surface finish accuracy.

By Application

Reverse EngineeringMetrology tools support accurate recreation of parts and models. Commonly used for legacy component digitization and design improvement. Quality Inspection

Ensures manufacturing precision and defect-free production. Plays a central role in compliance and certification processes. Industrial Automation

Integrated into smart manufacturing and robotics systems for real-time inspection and closed-loop quality control. Mapping and Topographic Measurement

Used across energy, construction, mining, and defense sectors for high-precision spatial measurement and surveying. Precision Engineering

Supports micro-level manufacturing applications where dimensional errors can affect safety, durability, or performance.

By End-User

AutomotiveAdopted for component standardization, assembly validation, and safety compliance across EVs and conventional vehicles. Aerospace and Defense

Used to maintain stringent material accuracy and tolerance requirements for critical components, structures, and assemblies. Semiconductor and Electronics

Ensures microscopic measurement accuracy for chips, sensors, circuits, and miniaturized components. Medical Devices and Healthcare

Supports precision manufacturing of implants, surgical tools, and diagnostic equipment with tight regulatory standards. Energy and Power

Measurement tools assist in inspecting turbines, pipelines, equipment, and large-scale industrial systems.

Regional Analysis

North AmericaStrong adoption driven by advanced aerospace, defense, and semiconductor sectors, along with major metrology technology providers. Europe

Dominated by automotive and aerospace industries with strict compliance regulations accelerating automation and precision measurement adoption. Asia-Pacific

Fastest growth due to large-scale electronics and automotive production, government industrialization programs, and rising R&D investments. Latin America

Steady growth led by automotive, energy, and manufacturing modernization initiatives, with increasing outsourcing of metrology services. Middle East & Africa

Emerging demand driven by infrastructure development, energy projects, and adoption of advanced quality assurance systems in manufacturing.

Top Key Players and Market Share Insights

FARO Technologies Nikon Metrology Carl Zeiss AG Hexagon AB Renishaw PLC Jenoptik AG Perceptron Automated Precision Inc. KLA Corporation Applied Materials Inc.

QBCFMonitorService Not Running Affects Network Performance

QBCFMonitorService Not Running Affects Network Performance