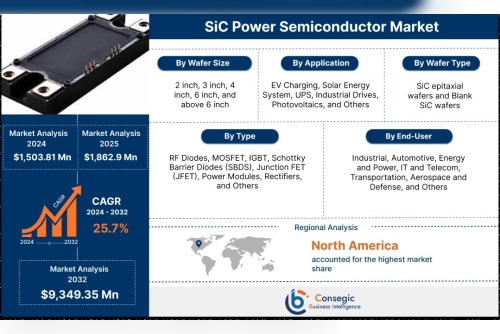

SiC Power Semiconductor Market

Introduction

The Silicon Carbide (SiC) power semiconductor market is rapidly emerging as a transformative force in the global electronics and energy sectors. SiC semiconductors, known for their superior properties such as high thermal conductivity, high breakdown voltage, and efficiency at high frequencies, are revolutionizing power management systems across various industries. These components are increasingly being adopted in electric vehicles (EVs), renewable energy systems, industrial equipment, and power grids due to their ability to operate at higher temperatures and voltages with reduced energy losses. As demand for energy-efficient solutions and compact power devices grows, the SiC power semiconductor market is poised for significant expansion, driven by technological advancements and a strong push toward sustainable energy and electrification trends.

SiC Power Semiconductor Market Size

SiC Power Semiconductor Market size is estimated to reach over USD 9,349.35 Million by 2032 from a value of USD 1,503.81 Million in 2024 and USD 1,862.90 Million in 2025, growing at a CAGR of 25.7% from 2025 to 2032.

Scope and Overview of the SiC Power Semiconductor Market

The SiC power semiconductor market encompasses a wide range of applications, technologies, and industries that leverage the unique advantages of silicon carbide materials for power conversion and control. This market includes various SiC-based devices such as MOSFETs, diodes, and modules, which are integral to high-performance power electronics. The scope of the market spans key sectors including automotive (especially electric vehicles), renewable energy (such as solar and wind power), industrial motor drives, aerospace, and power distribution systems. With increasing emphasis on energy efficiency, miniaturization, and sustainability, the demand for SiC power semiconductors is witnessing rapid growth globally. The market is further propelled by ongoing research and development, government incentives for clean energy adoption, and the rising need for high-power density solutions. As a result, the SiC power semiconductor market is set to play a crucial role in shaping the future of energy and electronic systems.

SiC Power Semiconductor Market Dynamics (DRO)

1. Drivers:

Rising Adoption of Electric Vehicles (EVs): SiC semiconductors improve efficiency, range, and charging speed in EV powertrains and charging infrastructure. Demand for Energy-Efficient Power Electronics: SiC devices offer lower energy losses and better thermal performance than traditional silicon-based semiconductors. Growth in Renewable Energy Installations: Increasing deployment of solar inverters and wind turbines is boosting demand for high-performance SiC power devices. Government Support and Regulations: Incentives for clean energy and stricter emission regulations are accelerating the shift toward SiC-based technologies. Advancements in SiC Manufacturing Technology: Improvements in wafer production and cost reduction are making SiC components more commercially viable.2. Restraints:

High Initial Cost of SiC Devices: Compared to silicon counterparts, SiC components are still more expensive, limiting adoption in cost-sensitive applications. Complex Fabrication and Material Challenges: Difficulties in manufacturing defect-free SiC wafers and devices pose technical barriers. Limited Supply Chain and Availability: A relatively small number of suppliers and limited capacity can create bottlenecks and increase lead times.3. Opportunities:

Expansion in 5G and Industrial Automation: SiC can support high-frequency, high-efficiency power systems required in advanced telecom and industrial applications. Emerging Markets and Electrification Initiatives: Rapid urbanization and infrastructure development in emerging economies are creating new opportunities for SiC solutions. Integration with Advanced Technologies: Potential integration with AI, IoT, and smart grid systems enhances the strategic value of SiC devices in modern electronics.

SiC Power Semiconductor Market Segmental Analysis

The SiC power semiconductor market is segmented across various dimensions to provide a comprehensive understanding of its structure and growth potential:

1. By Type:

SiC Discrete Devices: Includes SiC MOSFETs, diodes, and thyristors used in standalone applications. SiC Power Modules: Integrated solutions combining multiple SiC devices, typically used in high-power applications. Others: Emerging or hybrid types incorporating SiC with other materials or advanced packaging.2. By Wafer Size:

2-Inch 4-Inch 6-Inch 8-Inch and AboveThe industry is shifting toward larger wafer sizes (6-inch and 8-inch) to reduce costs and increase production efficiency.

3. By Wafer Type:

n-Type SiC Wafers: Commonly used for their electron mobility and efficiency in power switching. Semi-insulating SiC Wafers: Used in high-frequency and RF applications due to their electrical isolation capabilities.4. By Application:

Power Supplies and Inverters Motor Drives Battery Management Systems Electric Vehicle (EV) Components Renewable Energy Systems Industrial Equipment Others (e.g., Aerospace, Data Centers)5. By End-User:

Automotive Energy and Power Industrial Telecommunications Aerospace and Defense Consumer Electronics Others6. By Region:

North America: Strong presence of EV manufacturers and R&D facilities. Europe: High adoption in automotive and renewable sectors. Asia-Pacific: Fastest-growing market due to manufacturing hubs in China, Japan, South Korea, and India. Latin America: Emerging demand in energy and industrial sectors. Middle East & Africa: Gradual adoption in power infrastructure and renewable projects.Top Key Players & Market Share Insights

Infineon Technologies AG STMicroelectronics GeneSiC Semiconductor Inc. Semiconductor Components Industries, LLC NXP Semiconductors Texas Instruments Inc. Allegro MicroSystems, Inc. ROHM CO., LTD. WOLFSPEED, INC. TT Electronics Renesas Electronics Corporation

Contact Us:

Consegic Business intelligence

Email : [email protected]

Sales : [email protected]