Wafer Fabrication Market

Introduction

The wafer fabrication market plays a critical role in the global semiconductor industry, serving as the foundational stage in the production of integrated circuits (ICs). Wafer fabrication involves a series of complex processes including photolithography, doping, etching, and deposition, which are used to build electronic components onto silicon wafers. This market is driven by the rising demand for advanced electronic devices, increasing adoption of AI and IoT technologies, and the growing need for miniaturized, high-performance semiconductors in various end-use industries such as consumer electronics, automotive, healthcare, and telecommunications. As technology nodes continue to shrink and demand for high-speed processing increases, wafer fabrication facilities (fabs) are investing heavily in advanced manufacturing equipment and automation, further propelling market growth.

Wafer Fabrication Market Size

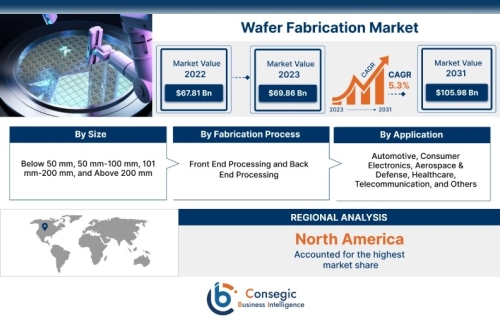

Wafer Fabrication Market size is estimated to reach over USD 108.37 Billion by 2032 from a value of USD 71.91 Billion in 2024 and is projected to grow by USD 74.41 Billion in 2025, growing at a CAGR of 5.3% from 2025 to 2032.

Wafer Fabrication Market Scope & Overview

The wafer fabrication market encompasses the processes, equipment, and technologies involved in the manufacturing of semiconductor wafers, which form the backbone of modern electronic devices. This market includes various stakeholders such as foundries, integrated device manufacturers (IDMs), and equipment suppliers. The scope of the market extends across multiple technology nodes, from legacy nodes used in automotive and industrial applications to advanced nodes required for high-end computing and AI chips. Key areas of focus include advancements in lithography, the adoption of EUV (Extreme Ultraviolet) technology, and the integration of novel materials to enhance chip performance. The market also covers geographical trends, with significant activities concentrated in regions like Asia-Pacific, North America, and Europe. With the growing reliance on semiconductors across emerging technologies and industries, the wafer fabrication market is poised for sustained expansion and innovation.

Wafer Fabrication Market Dynamics – (DRO)

Drivers:

Rising demand for consumer electronics and smart devices. Increased adoption of AI, IoT, and 5G technologies requiring advanced chips. Growth in the automotive sector, especially electric and autonomous vehicles. Surge in data centers and cloud computing applications. Technological advancements in wafer processing equipment and techniques.Restraints:

High capital investment and operational costs of wafer fabs. Supply chain disruptions and semiconductor material shortages. Technical challenges in transitioning to smaller nodes (e.g., below 5nm). Stringent environmental regulations impacting manufacturing processes.Opportunities:

Expansion of semiconductor manufacturing in emerging economies. Growing focus on chip customization for specific applications (e.g., AI, healthcare). Increased investment in R&D and government support for domestic chip production. Integration of new materials like silicon carbide (SiC) and gallium nitride (GaN) in fabrication.

Wafer Fabrication Market Segmental Analysis

By Size:

150 mm – Primarily used in legacy applications and mature semiconductor products. 200 mm – Common in analog, power, and MEMS devices due to cost-efficiency. 300 mm – Widely adopted for high-volume manufacturing of advanced ICs. 450 mm – Emerging size offering higher throughput, currently under development.By Fabrication Process:

Front-End-of-Line (FEOL) – Involves the creation of transistor structures on the wafer. Back-End-of-Line (BEOL) – Includes metal interconnect formation and insulation layers. Assembly & Packaging – Final steps where dies are cut, packaged, and tested for use.By Application:

Consumer Electronics – High demand for smartphones, tablets, and wearables drives growth. Automotive – Increasing semiconductor usage in EVs and ADAS systems. Industrial – Automation and Industry 4.0 boost demand for robust semiconductor solutions. Telecommunication – Supports 5G infrastructure and networking devices. Healthcare – Used in medical imaging, diagnostics, and wearable health devices. Others – Includes aerospace, defense, and other specialized sectors.By Region:

North America – Strong presence of fabless companies and technological innovators. Europe – Emphasis on automotive semiconductor production and R&D. Asia-Pacific – Dominates global production with key players in China, Taiwan, and South Korea. Latin America – Emerging market with increasing investments in electronics manufacturing. Middle East & Africa – Growing interest in developing semiconductor ecosystems.

Top Key Players & Market Share Insights

Taiwan Semiconductor Manufacturing Company Limited Tokyo Electron Limited Intel Corporation Lam Research Corporation Motorola Solutions Inc. Applied Materials Inc. KLA Corporation STMicroelectronics SOITEC Samsung

Consegic Business intelligence

Email : [email protected]

Sales : [email protected]