Global Buy Now Pay Later (BNPL) Market: Transforming Consumer Credit & Redefining Digital Commerce

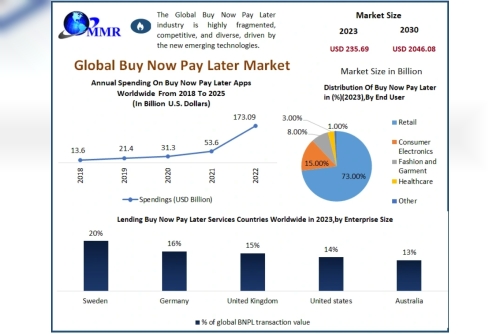

The Global Buy Now Pay Later (BNPL) Market, valued at USD 235.36 billion in 2023, is on track to witness explosive growth, projected to reach USD 2046.08 billion by 2030, expanding at a CAGR of 36.17%. As consumer behavior shifts toward flexible, transparent, and convenient financing solutions, BNPL continues to reshape the global payments landscape—becoming an essential component of modern retail ecosystems.

Introduction: The Rise of Flexible Consumer Lending

Buy Now Pay Later is a short-term, instalment-based financing method that enables consumers to split their purchases into smaller payments, usually interest-free. Initially targeted at millennials and Gen Z shoppers, BNPL has rapidly evolved into a mainstream payment method used across age groups and income levels. Its growing presence in both e-commerce and physical stores demonstrates how BNPL is bridging digital payments with traditional retail.

From everyday essentials to high-value items like electronics and fashion, BNPL offers customers a frictionless way to manage cash flows—fueling wider adoption globally. Businesses, meanwhile, leverage BNPL to boost cart conversions, expand customer base, and enhance loyalty.

To know the most attractive segments, click here for a free sample of the report:https://www.maximizemarketresearch.com/request-sample/118477/

Market Dynamics

BNPL is Redefining the Online Shopping ExperienceThe rapid digitalization of retail and a shift away from credit cards—particularly after pandemic-induced financial stress—have accelerated BNPL adoption. Consumers increasingly prefer predictable, interest-free payment plans over revolving credit lines.

Key demand drivers include:

Instant approvalsZero or minimal interestNo hidden chargesSimplified repayment schedulesShoppers also appreciate BNPL’s ease of use for impulse purchases or items that exceed their immediate budgets. As finance becomes more embedded into checkout journeys, BNPL is emerging as a preferred choice for digital-native consumers.

Debit Cards Dominate BNPL Installment PaymentsBNPL transactions are largely tied to debit cards, highlighting consumers' preference for transparency and controlled spending.

Share of BNPL Installments by Payment Method

Debit Cards: 90.4% (2023)Credit Cards: 10%ACH, Prepaid Cards & Checks: <1%The dominance of debit-based BNPL reflects a behavioural shift—consumers want flexibility without incurring future interest burdens. Through seamless verification systems, BNPL also ensures secure transactions, automatic deductions, and reduced lending risk.

Concerns Around Debt & Regulatory TighteningThe global rise of BNPL has prompted scrutiny from regulators, especially regarding:

Overspending by young consumersCredit stacking (credit used to pay for credit)Lack of transparency around late feesAbsence of formal credit assessmentsCountries like the UK, Australia, and regions in Europe are moving toward regulatory oversight. Future frameworks may include mandatory credit checks, standardized disclosures, stricter merchant onboarding, and caps on late fees.

As regulations mature, BNPL providers will need to emphasize financial literacy, responsible lending, and compliance-driven product innovation.

Market Trends

E-commerce Expansion Fueling BNPL GrowthThe surge in online retailing—across fashion, electronics, travel, health, and food delivery—is directly contributing to BNPL’s massive adoption. Rising smartphone penetration, digital banking, and faster checkout experiences continue to push BNPL deeper into tier-2 and tier-3 markets, especially in emerging economies.

BNPL as a Credit Access Tool for the UnderbankedIn developing markets like India, the Philippines, and parts of Southeast Asia, BNPL is becoming a stepping stone to formal credit. First-time borrowers, students, and young professionals prefer BNPL due to:

Minimal documentationInstant eligibilityNo credit history requirementIndia’s BNPL market alone is expected to grow from USD 3–3.5 billion to USD 60–65 billion by 2029.

Embedded Finance and omnichannel BNPLRetailers are integrating BNPL across physical stores, apps, marketplaces, and social commerce platforms, unlocking omnichannel shopping experiences. Partnerships between BNPL providers and merchants—from fashion brands to travel platforms—are creating high-conversion checkout ecosystems.

Segment Analysis

By Channel

Online (67.2% share in 2023)

Online BNPL leads due to:

E-commerce growthPost-pandemic payment shiftsGlobal partnerships (e.g., Uplift–Tripster)POS (In-store)

In-store BNPL is rising as retailers use instalment plans to drive customer loyalty and repeat purchases.

By Enterprise Size

Large Enterprises (61.37% in 2023)

Large enterprises leverage BNPL to enhance customer affordability and increase high-ticket sales.

SMEs

SMEs are the fastest-growing segment as BNPL helps:

Improve conversion ratesLower customer acquisition costsOffer transparent pricingBy End-User

Fashion & Garments (39.46% share)

Fashion brands widely adopt BNPL due to high purchase frequency and strong customer engagement.

Consumer Electronics

Expected to grow rapidly, supported by demand for smartphones, laptops, and other gadgets.

Other notable categories:

HealthcareRetailLeisure & EntertainmentTo know the most attractive segments, click here for a free sample of the report:https://www.maximizemarketresearch.com/request-sample/118477/

Regional Insights

North America (34.51% share in 2023)

The most mature BNPL market, driven by players like Affirm, Amazon Pay, PayPal, Sezzle, and Apple Pay. BNPL accounts for 5–7% of U.S. e-commerce transactions.

Asia Pacific

The fastest-growing region, supported by:

Rising digital paymentsGen Z adoptionExpanding e-commerce ecosystemsGrowing fintech innovationCountries like India, Singapore, Australia, and Japan are hotspots.

Europe

Strong growth driven by established players like Klarna, Clearpay, and Laybuy.

The UK alone accounts for 6–8% of e-commerce BNPL transactions.

Middle East, Africa & CIS

BNPL adoption is rising in:

UAESaudi ArabiaEgyptRussiaKazakhstanThe growth is propelled by young, tech-savvy populations and rising online transactions.

Competitive Landscape

The BNPL market is intensely competitive and innovation-driven. Companies focus on:

AI-powered risk assessmentResponsible lending frameworksLaunching interest-free instalment productsStrategic partnerships with banks and merchantsGlobal expansion through acquisitions and new product launchesKey Players Include:

US:

Affirm, ViaBill, Visa, Quadpay, Splitit, Mastercard, Sezzle, Perpay, Amazon, Apple Pay, PayPal, Revo

International:

Klarna (Sweden), Afterpay (Australia), Openpay (Australia), LatitudePay (Australia), Atome (Singapore), Hoolah (Singapore), Cashalo (Philippines), Paidy (Japan), PayBright (Canada), Carbon Zero (Canada), Clearbanc (Canada), Pine Labs (India)

Conclusion

The Buy Now Pay Later Market is entering a dynamic expansion phase, reshaped by digital commerce, financial inclusion, and innovative fintech solutions. Despite regulatory challenges, BNPL is poised to become a core pillar of global payments—transforming how consumers spend, how merchants sell, and how credit is accessed.

As technology advances and adoption deepens across sectors, the BNPL ecosystem is expected to play a pivotal role in the future of responsible, flexible, and customer-centric financing.

✅Pour l'amour d'un garçon

✅Pour l'amour d'un garçon