Global Managed Services Market: Growth, Trends, and Strategic Outlook

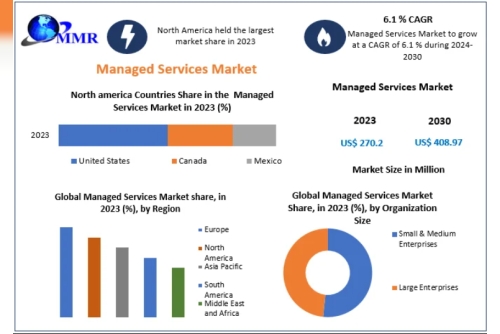

The Global Managed Services Market has emerged as a critical pillar of modern enterprise IT strategy. Valued at US$ 270.2 billion in 2023, the market is projected to expand steadily at a CAGR of 6.1% from 2023 to 2030, reaching an estimated US$ 408.97 billion by 2030. This growth reflects the increasing reliance of organizations on external expertise to manage complex and evolving IT environments efficiently.

Market Overview

Managed services involve the continuous management of an organization’s IT infrastructure and operations under predefined service level agreements (SLAs). These services allow enterprises to offload routine and specialized IT functions to third-party providers, enabling internal teams to focus on core business objectives.

The scope of managed services spans both on-premises and cloud-based environments, covering areas such as network management, cybersecurity, data centers, cloud infrastructure, and IT support. As businesses undergo rapid digital transformation, managed service providers (MSPs) play a crucial role in enhancing system performance, improving security, and ensuring operational continuity.

The Cloud, Hosting & Managed Services Market Monitor highlights how strategic collaboration with MSPs enables enterprises to remain resilient and competitive in an increasingly digital and interconnected business landscape.

Request a Free Sample Copy or View Report Summary:https://www.maximizemarketresearch.com/request-sample/3559/

Market Dynamics

Key Driver: Rising Complexity of IT Ecosystems

One of the primary drivers fueling the managed services market is the growing complexity of IT environments. Organizations today operate across a mix of on-premises infrastructure, public and private clouds, hybrid systems, and multiple applications. Managing these diverse components requires advanced expertise, continuous monitoring, and significant resources.

Additionally, the rapid evolution of cybersecurity threats—including ransomware, malware, and data breaches—has intensified the need for specialized security management. Businesses increasingly rely on managed security services to safeguard sensitive data and ensure regulatory compliance.

The widespread adoption of remote work and digital collaboration tools has further increased IT complexity. Employees accessing enterprise systems from various locations and devices create new challenges related to security, connectivity, and performance. Managed service providers address these challenges by offering remote IT support, secure access solutions, and unified communication platforms, thereby accelerating market growth.

Market Restraint: Lack of Standardization and Interoperability

Despite strong growth prospects, the managed services market faces constraints due to the absence of uniform standards and interoperability across service providers. Enterprises often struggle to integrate managed services with their existing IT infrastructure, leading to compatibility issues, operational inefficiencies, and higher costs.

The lack of common frameworks complicates data migration, workflow integration, and communication between disparate systems. This limitation restricts flexibility and scalability, making it difficult for organizations to adapt quickly to changing business needs or adopt emerging technologies.

To overcome these challenges, industry stakeholders must collaborate to develop standardized protocols and best practices, enabling smoother integration and wider adoption of managed services across diverse IT environments.

Market Opportunity: Expanding Adoption of Cloud Services

The accelerating shift toward cloud computing presents a major growth opportunity for the managed services market. Organizations are increasingly moving workloads to the cloud to benefit from scalability, flexibility, and cost efficiency. However, cloud migration and management require specialized skills, creating strong demand for managed cloud services.

Managed service providers assist enterprises throughout the cloud journey—ranging from cloud strategy and migration to infrastructure optimization, performance monitoring, and security management. They also enable seamless management of multi-cloud and hybrid cloud environments, ensuring consistent governance and compliance across platforms.

As cloud adoption continues to rise globally, managed services are positioned to play a central role in maximizing cloud value while minimizing operational risks.

Segment Analysis

By Deployment Mode

In 2023, the on-premises segment held the dominant share of the managed services market. Many organizations continue to rely on existing investments in physical infrastructure such as servers, networking equipment, and data centers. For industries like banking, healthcare, and government, on-premises deployment offers greater control over sensitive data and compliance requirements.

Legacy systems that are not easily migrated to the cloud also support the dominance of on-premises solutions. Moreover, applications requiring low latency and high performance often perform better in on-premises environments. Managed service providers offer customized solutions to optimize security, performance, and cost efficiency for these deployments.

Regional Analysis

North America: Market Leader

North America accounted for the largest share of the global managed services market in 2023. The region benefits from a highly advanced IT ecosystem, with enterprises across industries heavily dependent on sophisticated digital infrastructure.

The presence of leading global MSPs, combined with strong innovation capabilities and a skilled workforce, has positioned North America at the forefront of managed services adoption. Regulatory requirements in sectors such as healthcare, finance, and public services further drive demand for managed IT and security solutions.

As a result, North America continues to set industry benchmarks, influence market trends, and drive innovation in managed services worldwide.

Market Scope and Segmentation

By Service Type

Managed Network ServicesManaged Information ServicesManaged Security ServicesManaged Data Center ServicesManaged Mobility ServicesManaged IT Infrastructure ServicesBy Deployment Mode

CloudOn-PremisesBy Organization Size

Small & Medium EnterprisesLarge EnterprisesBy Vertical

BFSIConsumer Goods & RetailManufacturingHealthcare & Life SciencesMedia & EntertainmentTelecom & ITGovernment & Public SectorEnergy & UtilitiesEducationOthersBy Region

North AmericaEuropeAsia PacificMiddle East & AfricaSouth AmericaRequest a Free Sample Copy or View Report Summary:https://www.maximizemarketresearch.com/request-sample/3559/

Competitive Landscape

The managed services market is highly competitive, with global and regional players focusing on innovation, strategic partnerships, and service expansion.

Key Players Include:

North America

IBMAccentureHewlett Packard Enterprise (HPE)Cisco SystemsDXC TechnologyRackspace TechnologyDeloitteCognizantEurope

AtosCapgeminiAccentureEricssonAsia Pacific

FujitsuNTT Ltd.WiproInfosysHCL TechnologiesTata Consultancy Services (TCS)Conclusion

The global managed services market is on a strong growth trajectory, driven by rising IT complexity, cybersecurity concerns, and accelerating cloud adoption. While challenges related to standardization persist, ongoing innovation and industry collaboration are expected to unlock new opportunities. As enterprises continue to prioritize efficiency, security, and scalability, managed services will remain a cornerstone of modern digital transformation strategies.