According to a recent report by Grand View Research, Inc., the Europe veterinary pharmaceuticals market is projected to reach USD 11.85 billion by 2030, growing at a compound annual growth rate (CAGR) of 7.3% from 2023 to 2030. Key drivers of this growth include increasing demand for companion animal products, rising pet-related expenditures, a growing prevalence of diseases in both companion and livestock animals, and proactive efforts by industry participants. For example, in September 2020, Boehringer Ingelheim partnered with the Fraunhofer Institute for Molecular Biology and Applied Ecology IME to develop sustainable, effective veterinary antiparasitic solutions.

The COVID-19 pandemic had a notable impact on the market, causing supply chain disruptions and a drop in sales for many companies. Additionally, the pandemic led to reduced R&D efforts, lower demand, and operational challenges stemming from evolving regulations and restrictions. In response, governments, regulatory authorities, and companies implemented various recovery strategies, including relaxed restrictions, financial stimulus packages, policy adjustments, and conditional exemptions. One such measure was the European Medicines Agency’s (EMA) decision to extend the validity of GMP certificates until the end of 2021, eliminating the need for further action by the certificate holders. This applied to manufacturing and import sites of both active substances and finished veterinary products within the EEA.

To ensure veterinary medicines remained accessible in EU Member States, adjustments were made to product information and labeling requirements. For instance, under Article 61(1) of Directive 2001/82/EC, exemptions were granted during the pandemic, such as allowing product labels not to be translated into the official national languages.

The expanding pet population and growing spending on pets have significantly boosted demand for companion animal products, including pet food, veterinary medications, and services. This upward trend is expected to continue throughout the forecast period. As an illustration, a 2020 FEDIAF report estimated annual pet food sales at approximately EUR 21.8 billion. Additionally, an increase in single-person and small households, alongside an aging population across Europe, is contributing to higher pet ownership. The COVID-19 pandemic further accelerated this trend, with a January 2021 report by Deutsche Welle highlighting a sharp rise in pet adoption in Germany.

Get a preview of the latest developments in the Europe Veterinary Pharmaceuticals Market! Download your FREE sample PDF today and explore key data and trends

The competitive landscape of the European veterinary pharmaceuticals market is anticipated to remain intense over the coming years. The market features a mix of numerous small and large players, resulting in stiff competition, particularly among smaller companies vying to maintain their market share. Businesses are increasingly pursuing strategies such as mergers and acquisitions, product launches, and regional expansion to enhance their market presence. For example, in August 2021, Elanco advanced its growth strategy in the pet health sector by acquiring Kindred Biosciences, thereby supporting its Innovation, Portfolio, & Productivity (IPP) strategy. The acquisition brought three potential blockbuster dermatology treatments—expected to launch by 2025—into Elanco’s pipeline.

Highlights of the Europe Veterinary Pharmaceuticals Market Report:Innovation will remain a key market driver, with ongoing mergers, acquisitions, and strategic partnerships.

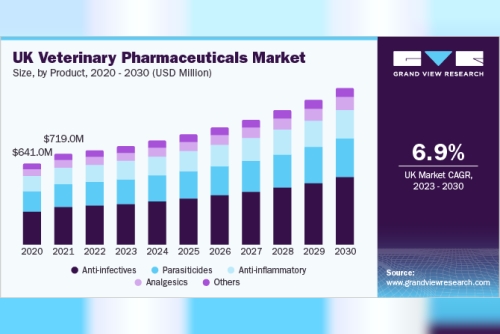

The anti-infective segment accounted for the highest revenue share in 2022, driven by the increased incidence of bacterial, viral, and fungal infections in pets.

Efforts to minimize parasitic infections in livestock—crucial for securing the food supply—are expected to further stimulate market growth.

Demand for companion animal pharmaceuticals is set to rise, fueled by the expanding pet population and increased awareness of zoonotic diseases following the COVID-19 outbreak.

Companies are actively investing in R&D to develop both new and existing products aimed at improving animal health outcomes.

For instance, Dechra Pharmaceuticals launched 15 products in 2019 through its Le Vet pipeline, while Norbrook initiated 5 R&D projects in 2020, with plans for 10 additional developments within two years.

Leading Companies in the Europe Veterinary Pharmaceuticals Market:Merck & Co., Inc.

Ceva

Vetoquinol

Zoetis Services LLC

Boehringer Ingelheim International GmbH

Elanco

Virbac

Calier

Bimeda Corporate

Gather more insights about the market drivers, restrains and growth of the Europe Veterinary Pharmaceuticals Market