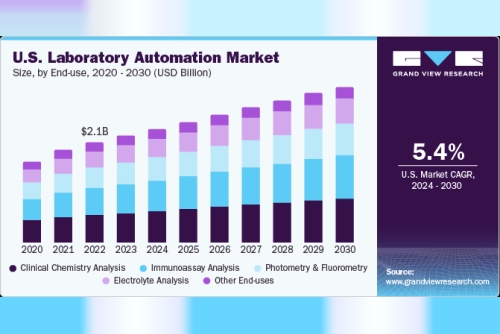

The U.S. laboratory automation market size was estimated at USD 2.18 billion in 2023 and is expected to grow a CAGR of 5.40% from 2024 to 2030. Key factors contributing to this market growth include the local presence of major key companies, easy availability of fully automated laboratory solutions, higher adoption of laboratory automation, and launch of newer solutions. The U.S. laboratory automation market dominated the global laboratory automation market in 2023, accounting for nearly 30% of the total revenue generated. The region benefits from a robust healthcare infrastructure, fostering the uptake of laboratory automation systems. The presence of key companies and favorable reimbursement structures further propel the integration of innovative automation solutions. Rising cases of chronic and infectious diseases drive the demand for laboratory automation, fueling market expansion.

The U.S. government’s focus on technological progress and the rise in research and development funding fosters an environment that enables manufacturers of laboratory automation to utilize state-of-the-art technologies and maintain their competitiveness in the international market. Technological advancements pertinent to pharmaceutical laboratories and rising demand for laboratory automation are expected to fuel the demand for these systems in the coming years.

Furthermore, advancements in R&D labs, especially in pharmaceutical and biotechnological laboratories, will likely bolster market growth. A growing focus on improving the efficiency of laboratories is also poised to help the market gain tremendous momentum over the coming years. The use of Laboratory Information Management Systems in biobanking is on the rise. These systems are crucial for efficiently managing and tracking various aspects such as data quality, security measures, end-user billing, and patient demographic information. They also enhance the integration of data sampling and research information, simplifying data accessibility. Thus, the low implementation cost, efficient time management, and compliance with GDP, GCP, and GMP principles are key factors escalating market demand.

Gather more insights about the market drivers, restrains and growth of the U.S. Laboratory Automation Market

The industry exhibits a high degree of innovation driven by rapid technological advancements and a focus on research and development. Businesses are incorporating artificial intelligence, machine learning, and cloud technologies into their automation workflows to boost efficiency, data analytics abilities, and decision-making procedures. Innovation in the industry is prioritized to remain competitive and cater to changing demands.

Mergers and acquisitions play a significant role, heading towards industry consolidation and portfolio diversification. Recent strategic acquisitions by key companies such as Thermo Fisher Scientific Inc., Siemens Healthineers AG, and other industry giants aim to drive innovation, expand product portfolios, and contribute to the competitive landscape. For instance, in September 2023, Takara Bio and Eppendorf announced a strategic partnership to automate Takara Bio’s chemistries on Eppendorf’s platforms, aiming to enhance lab efficiency and reliability.

Adherence to governmental rules, industry norms, and customer demands is vital for manufacturers to guarantee the quality, safety, and industry competitiveness of their products. For example, the U.S. National Institute for Occupational Safety and Health published a blog post in 2015 to create guidelines to safeguard interactions between humans and robots.

The industry is focused on developing innovative automation systems, liquid handling solutions, robotic arms, and software applications to enhance laboratory processes. This emphasis on product development aligns with the industry’s drive for technological advancements, efficiency, and accuracy in laboratory operations.

Many industry players are expanding across the West Coast, East Coast, Midwest, and South, and each region’s concentration of laboratories, research institutes, and pharmaceutical companies contributes to industry growth. This strategic expansion allows companies to tap into diverse industries, collaborate with local institutions, and cater to specific regional demands, enhancing their industry reach and competitiveness. For instance, in February 2023, Automata, a leader in laboratory automation, expanded into the U.S. industry. This expansion, following their success in the UK, marked a significant step in the company’s global evolution.

Key U.S. Laboratory Automation Company Insights

The market is marked by a substantial degree of fragmentation, providing a wide array of opportunities for expansion and innovation, numerous competitors vying for higher market shares. Some companies in the U.S. laboratory automation market are QIAGEN; PerkinElmer Inc.; Thermo Fisher Scientific, Inc.; Siemens Healthcare GmbH; and Danaher.

Key market participants strive to outdo each other through product innovation, collaborations, and mergers, reflecting a vibrant and competitive market landscape. For instance, in January 2023, Helix and QIAGEN formed a strategic partnership to develop companion diagnostics for hereditary diseases. The partnership aimed to address health burdens in neuro-degenerative, cardiovascular, and auto-immune diseases.

Key U.S. Laboratory Automation Companies:

QIAGENPerkinElmer Inc.Thermo Fisher Scientific, Inc.Siemens Healthcare GmbHDanaherAgilent Technologies, Inc.Eppendorf SEHudson RoboticsAurora Biomed Inc.BMG LABTECH GmbHTecan Trading AGHamilton CompanyHoffmann-La Roche LtdOrder a free sample PDF of the U.S. Laboratory Automation Market Intelligence Study, published by Grand View Research.