Speed Sensor Market

Introduction

The speed sensor market plays a critical role in modern industrial, automotive, aerospace, and consumer electronics sectors by enabling precise measurement of rotational or linear speed. Speed sensors are essential components in systems that require accurate speed monitoring and control, including anti-lock braking systems (ABS), engine management systems, robotics, and conveyor systems. The market has witnessed steady growth, driven by the increasing demand for automation, advanced safety features in vehicles, and the proliferation of smart technologies. Technological advancements such as the integration of IoT, miniaturization of sensors, and development of wireless and contactless speed sensors are further propelling market expansion. With the automotive industry undergoing rapid transformation due to electrification and autonomous vehicle development, speed sensors are expected to remain a vital element in ensuring performance, safety, and efficiency.

Speed Sensor Market size

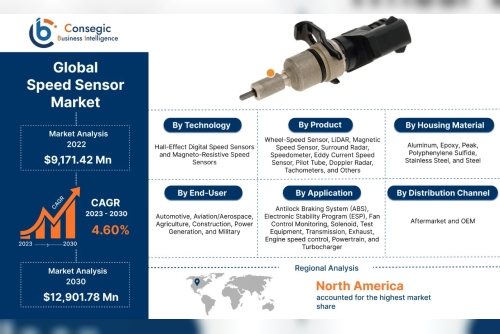

Speed Sensor Market is estimated to reach over USD 12,901.78 Million by 2030 from a value of USD 9,171.42 Million in 2022, growing at a CAGR of 4.60% from 2023 to 2030.

Speed Sensor Market: Scope & Overview

Market Scope

The speed sensor market encompasses the design, manufacturing, and application of sensors that detect and measure the speed of an object, typically in linear or rotational motion. These sensors are integral to a wide range of industries including automotive, aerospace, industrial automation, healthcare, and consumer electronics. The market includes various sensor types such as magnetic, Hall-effect, optical, and capacitive speed sensors, with applications in both contact and non-contact speed measurement systems.

Market Overview

The global speed sensor market is experiencing robust growth due to rising demand for real-time monitoring and safety technologies in automotive and industrial applications. In the automotive sector, speed sensors are crucial for advanced driver assistance systems (ADAS), electric vehicle (EV) components, and engine control. Similarly, industrial automation relies heavily on speed sensing for precision, efficiency, and safety in processes.

Speed Sensor Market Dynamics (DRO)

1. Drivers

Growing Automotive Industry: The increasing demand for vehicles equipped with advanced safety systems (e.g., ABS, traction control, ADAS) is driving the need for high-performance speed sensors. Industrial Automation and Industry 4.0: Adoption of smart manufacturing processes and automated machinery requires precise speed monitoring, boosting sensor deployment in industrial environments. Rise in Electric Vehicles (EVs): EVs and hybrid vehicles rely heavily on speed sensors for motor control, battery management, and regenerative braking systems. Technological Advancements: Innovations such as IoT-enabled sensors, wireless communication, miniaturization, and increased sensor durability are expanding the application base. Stringent Safety and Emission Regulations: Government mandates worldwide are pushing for improved vehicle safety and efficiency, increasing the integration of speed sensors in compliance systems.2. Restraints

High Cost of Advanced Sensors: Sophisticated sensor technologies can be expensive, limiting adoption in cost-sensitive markets or low-margin products. Technical Challenges in Harsh Environments: Maintaining sensor accuracy and reliability in extreme conditions (e.g., high temperatures, vibrations, corrosive environments) remains a challenge. Compatibility and Standardization Issues: Integrating speed sensors with various systems and platforms may require customization and increase complexity.3. Opportunities

Expansion in Emerging Economies: Rapid industrialization and urbanization in regions like Asia Pacific, Latin America, and Africa are opening new markets for speed sensor applications. Integration with AI and Predictive Maintenance Systems: Speed sensors can contribute valuable real-time data for machine learning models and condition-based monitoring in smart systems. Adoption in New Sectors: Healthcare devices, sports technology, and consumer wearables present untapped potential for speed sensors in monitoring movement and performance.

Speed Sensor Market Segmental Analysis

1. By Product

Magnetic Speed SensorsWidely used in automotive and industrial applications due to their robustness and ability to operate in harsh environments. Hall Effect Sensors

Known for high accuracy and reliability, especially in automotive and motor control applications. Optical Speed Sensors

Used where high precision is required, such as robotics and aerospace. Inductive Speed Sensors

Common in heavy-duty applications like railways, construction machinery, and manufacturing. Capacitive Speed Sensors

Suitable for non-contact applications and environments requiring high sensitivity.

2. By Technology

Contact Speed SensorsTraditional sensors where physical contact is required, often used in industrial settings. Non-Contact Speed Sensors

Preferred in modern applications for durability and reduced maintenance (e.g., automotive and medical devices).

3. By Housing Material

PlasticLightweight and cost-effective, often used in consumer electronics and light-duty industrial applications. Stainless Steel

Offers durability and corrosion resistance for harsh or outdoor environments. Aluminum

Combines light weight with adequate strength, common in automotive and aerospace sectors.

4. By Distribution Channel

OEMs (Original Equipment Manufacturers)Major share due to direct integration in vehicles, machinery, and equipment. Aftermarket

Significant in automotive and industrial replacement needs. Online Retailers

Growing channel, especially for low-cost or consumer-grade sensors. Distributors/Wholesalers

Traditional supply chain partners in industrial and automotive markets.

5. By Application

Engine and Transmission SystemsCritical in automotive applications for performance monitoring and control. Anti-lock Braking Systems (ABS)

Key safety application across all vehicle segments. Conveyor Systems

Widely used in industrial automation and logistics. Motorsports and Performance Vehicles

Demand high-speed and precision sensing. Consumer Electronics

Emerging application in smart gadgets and fitness equipment.

6. By End-User

AutomotiveThe largest end-user segment, including both traditional and electric vehicles. Industrial

Covers manufacturing, robotics, and automation. Aerospace & Defense

Requires high-performance and highly reliable sensors. Healthcare

Utilized in medical equipment for movement and flow rate sensing. Consumer Electronics

Smaller but growing segment with opportunities in wearables and sports equipment.

7. By Region

North AmericaMature market with strong presence in automotive and aerospace industries. Europe

Driven by strict safety and emission norms; major players include Germany, UK, and France. Asia-Pacific

Fastest-growing region, fueled by automotive production and industrial development, particularly in China, India, Japan, and South Korea. Latin America

Moderate growth with expanding industrial base. Middle East & Africa

Emerging opportunities in oil & gas, transportation, and infrastructure.

Top Key Players & Market Share Insights

Robert Bosch GmbH Honeywell International Inc. Continental AG Infineon Technologies AG Ford Motor Company Electro Sensors Inc. Standard Motor Products, Inc. TE Connectivity ABB NXP Semiconductors Siemens

Contact Us:

Consegic Business intelligence

Email : [email protected]

Sales : [email protected]

Rent A Cozy Fully Furnished Two Room Apartment in Bashundhara R/A.

Rent A Cozy Fully Furnished Two Room Apartment in Bashundhara R/A.